| Monthly Dividend Safety Analysis")

Up to date on October twenty fourth, 2025 by Bob Ciura

Enterprise Growth Corporations — or BDCs, for brief — permit buyers to generate revenue with the potential for sturdy whole returns whereas minimizing the tax paid on the company stage.

Regardless of these benefits, buyers typically keep away from enterprise improvement firms. This can be as a result of tax implications of their distributions for his or her shareholders. However even with the added headache come tax time, BDCs can nonetheless be worthwhile for revenue buyers.

Prospect Capital Company (PSEC) is without doubt one of the extra enticing enterprise improvement firms out there right now.

Prospect stands out from the group in that it pays month-to-month dividends, giving its shareholders a gentle and predictable passive revenue stream, which is extremely interesting to revenue buyers.

There are at the moment simply 78 month-to-month dividend shares. You possibly can obtain our full Excel spreadsheet of all month-to-month dividend shares (together with metrics that matter, like dividend yield and payout ratio) by clicking on the hyperlink beneath:

| Monthly Dividend Safety Analysis")

Prospect Capital’s dividend yield is over 19%, greater than ten instances that of the common S&P 500 Index. Our full record of shares with 5%+ dividend yields is right here.

Prospect’s excessive dividend yield and month-to-month dividend funds are two of the the explanation why the corporate deserves additional analysis. This text will focus on the funding prospects of Prospect Capital Company intimately.

Enterprise Overview

Prospect Capital Company is a Enterprise Growth Firm based in 2004. It is without doubt one of the largest, with a market cap of virtually $1.3 billion.

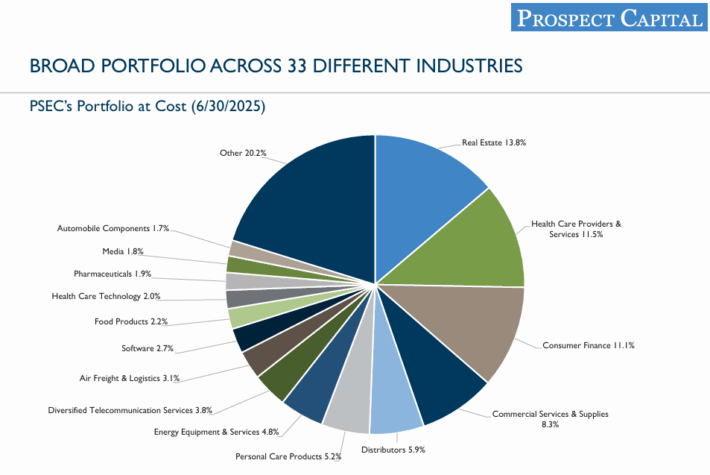

Prospect Capital is a number one supplier of personal fairness and personal debt financing for middle-market firms, broadly outlined as an organization with between 100 and a couple of,000 workers.

Prospect Capital advantages from working within the center market as a result of it lacks competitors from bigger, extra established lenders.

Supply: Investor Presentation

Center-market firms are typically too small to be prospects of economic banks however too massive to be served by the small enterprise representatives of retail banks. Prospect Capital does enterprise within the “candy spot” between these two providers. This lack of competitors on this sector has allowed Prospect Capital to finance some actually enticing offers.

Buyers ought to be aware that Prospect Capital is extremely uncovered to risky rates of interest. It is because the corporate’s liabilities are practically all at fastened charges, whereas its investments are practically all floating-rate devices. Which means curiosity expense is essentially fastened, whereas curiosity revenue rises and falls commensurately with prevailing rates of interest.

As rates of interest rise, the revenues from Prospects floating-rate interest-bearing belongings will enhance. On the identical time, Prospect’s curiosity expense will stay fixed since most of its debt is fastened. After all, the other is true, as falling charges typically imply declining curiosity revenue.

This makes Prospect Capital an incredible portfolio hedge towards interest-sensitive securities like REITs and utilities, nevertheless it underperforms when charges are very low and when charges are declining.

Prospect Capital’s versatile origination combine can also be a significant optimistic from an investor’s perspective, provided that the wide range of devices it makes use of to supply revenue helps it discover the perfect alternatives.

The corporate has many alternative methods to take a position with goal firms, together with various kinds of debt and fairness. All of them have completely different threat ranges and charges of return.

Prospect Capital’s willingness to hunt out the perfect devices — and having the dimensions to take action — is a significant benefit over different middle-market BDCs. The corporate’s funding technique is central to its long-term development.

Progress Prospects

Prospect Capital’s development prospects stem largely from the corporate’s capability to:

Elevate new capital by way of debt or fairness choices

Make investments this new capital in deal originations with an inner charge of return increased than the price of capital raised in Step 1

Prospect’s capability to supply new offers that supply acceptable risk-adjusted returns is a very powerful a part of this course of.

Happily for the corporate (and its buyers), there isn’t any scarcity of recent offers for Prospect’s consideration. The corporate has 1000’s of deal alternatives every year, permitting it to be very selective in its funding decision-making.

Prospect posted fourth quarter and full-year outcomes on August twenty sixth, 2025, and outcomes had been weak as soon as once more as the corporate continues to wrestle. Web curiosity revenue for the quarter was 17 cents per share. NII was down from 25 cents from the identical interval a yr in the past. Complete income plummeted 21% year-over-year to $167 million.

Complete originations had been $271 million, up from $196 million within the prior quarter. Complete repayments and gross sales had been $445 million, up from simply $192 million in Q3. Web originations, then, fell from $4 million in Q3 to -$175 million within the last quarter of the yr, shrinking the corporate’s portfolio to $6.67 billion. That’s down from $7.72 billion a yr in the past.

Annualized present yield for all investments rose to 9.6% from 9.2% in Q3, however decrease from 9.8% a yr in the past. Nonaccrual loans had been 0.3% of whole belongings from 0.6% in Q3. NAV was $6.56 per share, down from $7.25 in Q3 and $8.74 in final yr’s This autumn.

Dividend Evaluation

Prospect Capital’s dividend is the plain motive buyers would select to personal the inventory, so it’s crucial that the dividend is as protected as potential. As a BDC, Prospect Capital has no selection however to distribute primarily all of its taxable revenue to shareholders. Due to this, its payout ratio will all the time be very excessive and typically variable.

In different phrases, the dividend is definitely coated by internet funding revenue and has been for a while, which means the payout ought to be comparatively protected, barring a large affect from any potential financial downturn.

The corporate has declared 4.6 billion in cumulative distributions to shareholders since its IPO.

Clearly, the draw for Prospect Capital is in its capability to generate money to return to shareholders, and over time, it has executed that effectively.

The dividend seems protected for now, however buyers ought to constantly monitor the corporate’s internet funding revenue for any indicators of hassle that would probably result in additional cuts down the highway.

Associated: 3 Causes Why Corporations Reduce Their Dividends (With Examples)

Last Ideas

Prospect Capital’s excessive dividend yield and month-to-month distributions are two of the principle causes an investor would possibly take an curiosity on this inventory.

Taking a more in-depth look reveals that this BDC has a high-caliber management workforce and has positioned itself to thrive in most environments.

Nevertheless, the dividend seems to be on shaky monetary floor, which means Prospect is barely value a search for these buyers looking for excessive ranges of present revenue and month-to-month funds, plus abdomen the inherent dangers of proudly owning a BDC.

Don’t miss the assets beneath for extra month-to-month dividend inventory investing analysis.

And see the assets beneath for extra compelling funding concepts for dividend development shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to assist@suredividend.com.

– Neural Networks – 4 November 2025")

{kind=link}