Kenya’s monetary panorama stands as probably the most dynamic in Africa, pushed by speedy digitization, excessive cellular cash adoption, and continued efforts towards monetary inclusion. The nation is globally acknowledged for the success of M-Pesa, which has remodeled the best way Kenyans ship, obtain, and retailer cash since its launch in 2007. Immediately, cellular cash platforms are utilized by over 90% of adults, enabling seamless funds, financial savings, and entry to credit score.

In line with the FinAccess Family Survey 2024, 84.8% of Kenyan adults now have entry to formal monetary companies, marking a major milestone in inclusion. The Central Financial institution of Kenya’s Monetary Sector Stability Report 2024 additional notes the rising function of digital lending, with non-bank credit score suppliers and cellular mortgage apps turning into key sources of short-term finance, although considerations stay over affordability, information privateness, and client safety.

This Kenya-focused research varieties a part of a broader Sub-Saharan Africa Monetary Companies and Utilization Report, which examined evolving monetary behaviors throughout a number of African markets. Powered by TuuCho; GeoPoll performed the research by way of GeoPoll’s software and cellular internet platform, reaching a complete of two,500 respondents, providing a complete snapshot of how Kenyans entry, use, and understand monetary companies, from cellular wallets to conventional banking and rising credit score options. By situating Kenya’s findings inside the regional context, the report highlights each the nation’s management in digital finance innovation and the continued have to steadiness accessibility with accountable lending and monetary literacy.

Demographic Overview

The survey gathered responses from a various group of younger Kenyans, with most aged between 25 and 34 years (52%). Males accounted for 64% of respondents and females 36%, with a majority residing in city areas (73%) in comparison with rural areas (27%). When it comes to earnings, most respondents fall inside decrease to mid-income brackets, reflecting the significance of inexpensive monetary options. About 34% earn between KES 10,000 and 35,000 per 30 days, whereas 31% earn beneath KES 10,000. A smaller however rising middle-income phase, representing 15%, earns between KES 35,000 and 50,000 month-to-month.

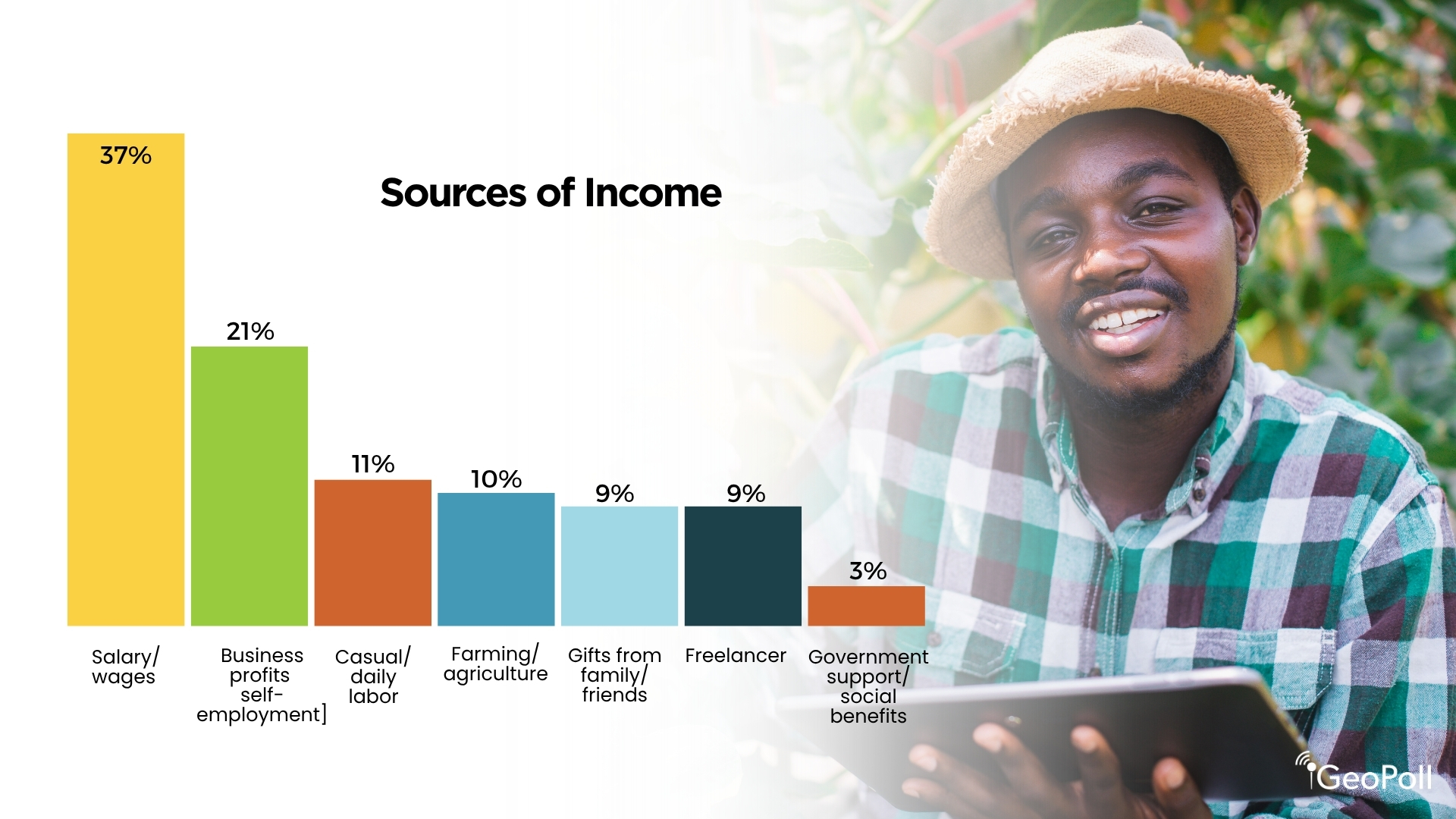

Sources of Revenue

The info signifies that almost all Kenyans derive their earnings from formal employment and small companies, reflecting a combined however evolving labor panorama. A major 37% of respondents earn their major earnings via salaries or wages from formal employment, exhibiting the continued significance of structured jobs, notably in city facilities. The second-largest supply of earnings is enterprise income or self-employment, reported by 21% of respondents, highlighting Kenya’s robust entrepreneurial tradition and the function of micro, small, and medium enterprises in sustaining livelihoods. Informal or every day labor ranks third at 11%, pointing to a sizeable portion of the inhabitants engaged in casual or short-term work.

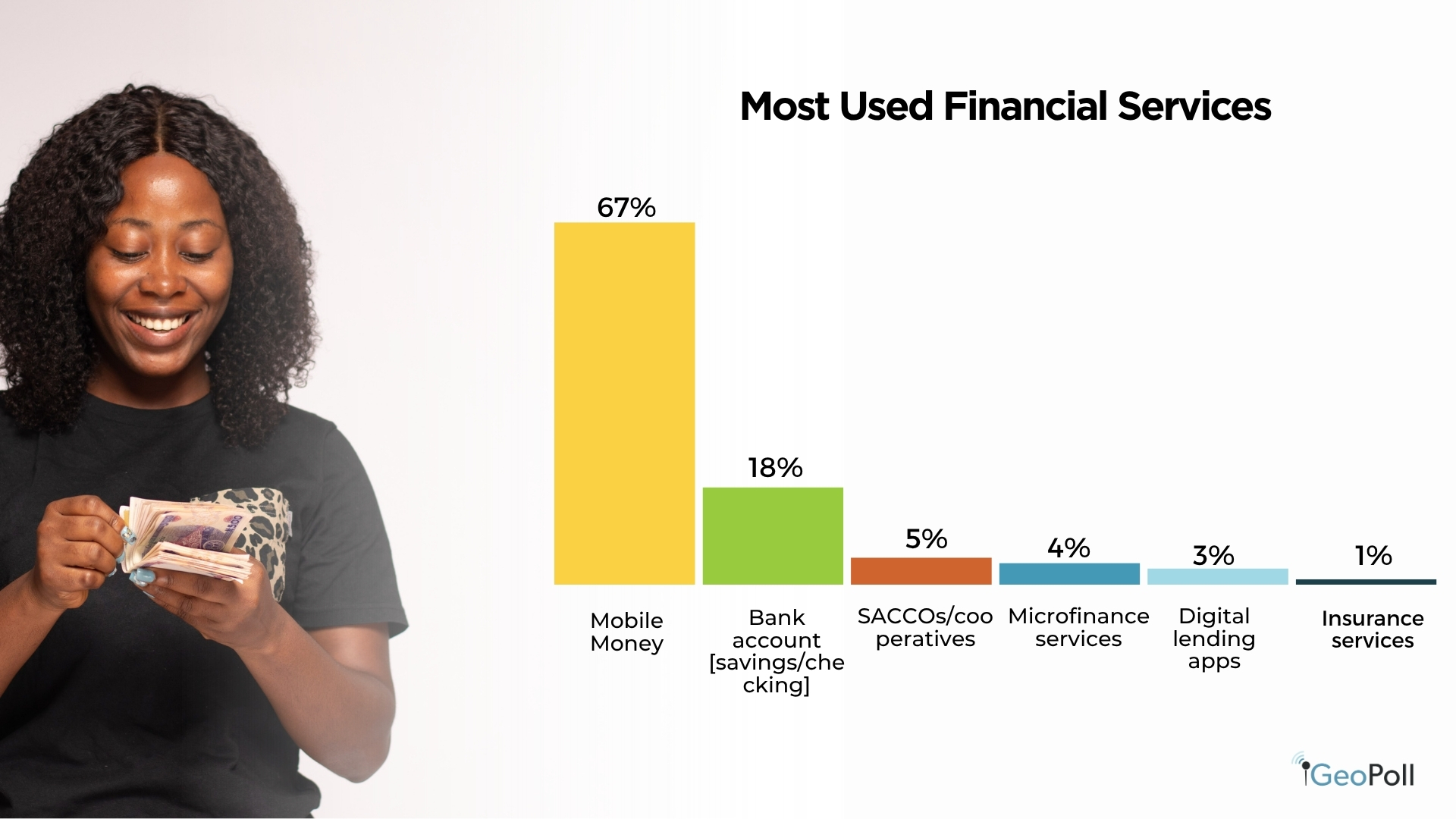

Monetary Service Utilization in Kenya

The findings reveal that cellular cash platforms stay the dominant monetary service in Kenya, reflecting their central function in on a regular basis transactions and monetary inclusion. About 67% of respondents reported utilizing cellular cash companies similar to M-Pesa, far surpassing all different monetary channels. This demonstrates the continued integration of cellular finance into each private and enterprise actions throughout the nation. The second most used service is financial institution accounts (together with financial savings and checking), cited by 18% of respondents, exhibiting that whereas conventional banking stays necessary, it lags behind mobile-based options in accessibility and utilization. SACCOs and cooperatives comply with distantly at 5%, indicating their area of interest however trusted function, notably in rural and community-based monetary techniques. The comparatively low adoption of microfinance companies (4%), digital lending apps (3%), and insurance coverage companies (1%) factors to alternatives for development in formal and digital finance past funds, particularly in credit score, financial savings, and danger safety merchandise.

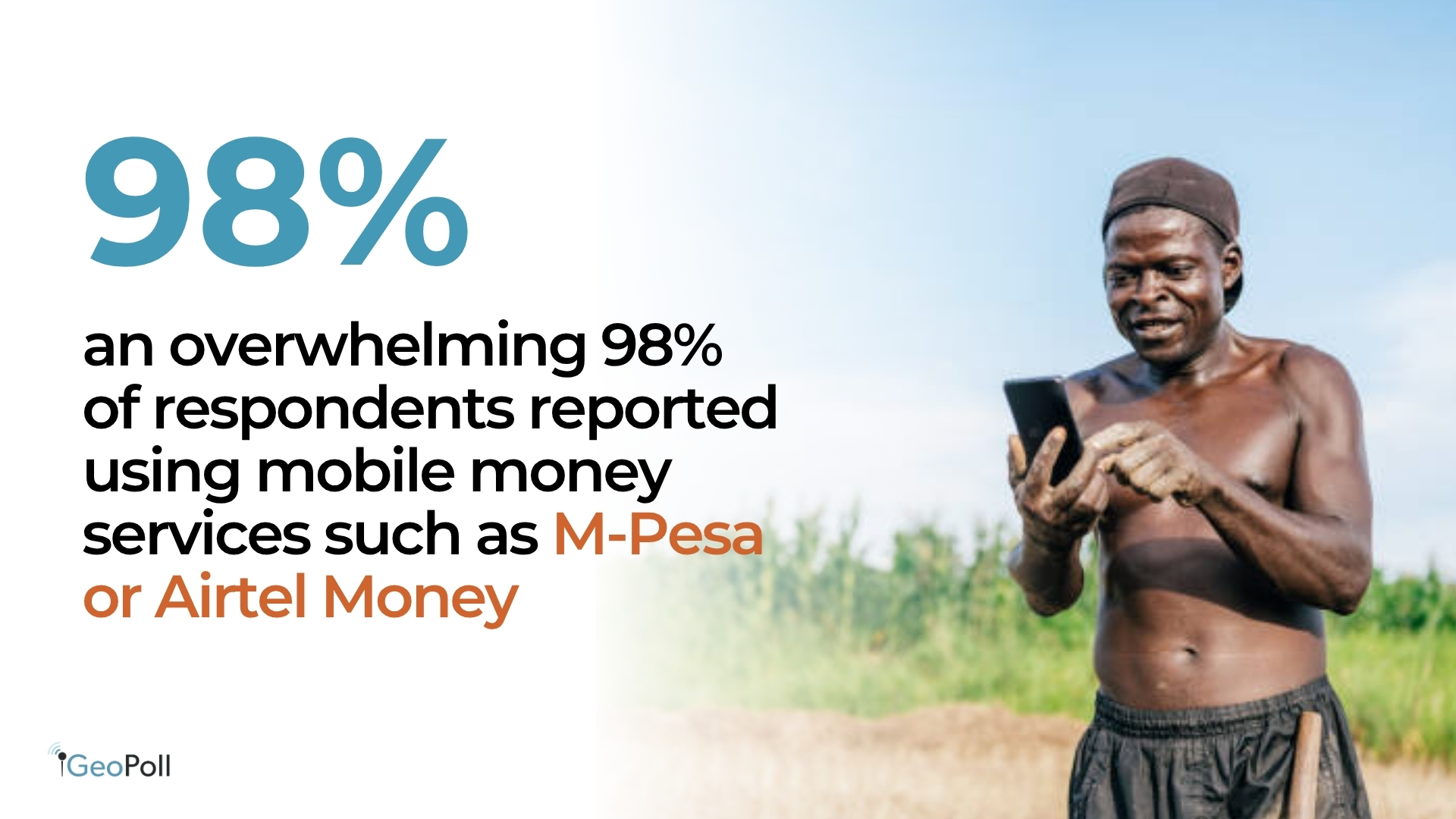

Cellular Cash Utilization in Kenya

Cellular cash continues to outline Kenya’s monetary panorama, reaching near-universal adoption. In line with the survey, an amazing 98% of respondents reported utilizing cellular cash companies similar to M-Pesa or Airtel Cash, confirming its place because the nation’s dominant monetary device. This near-total penetration displays how cellular wallets have turn out to be deeply embedded in every day monetary exercise, bridging gaps in formal banking entry and enabling real-time transactions for thousands and thousands.

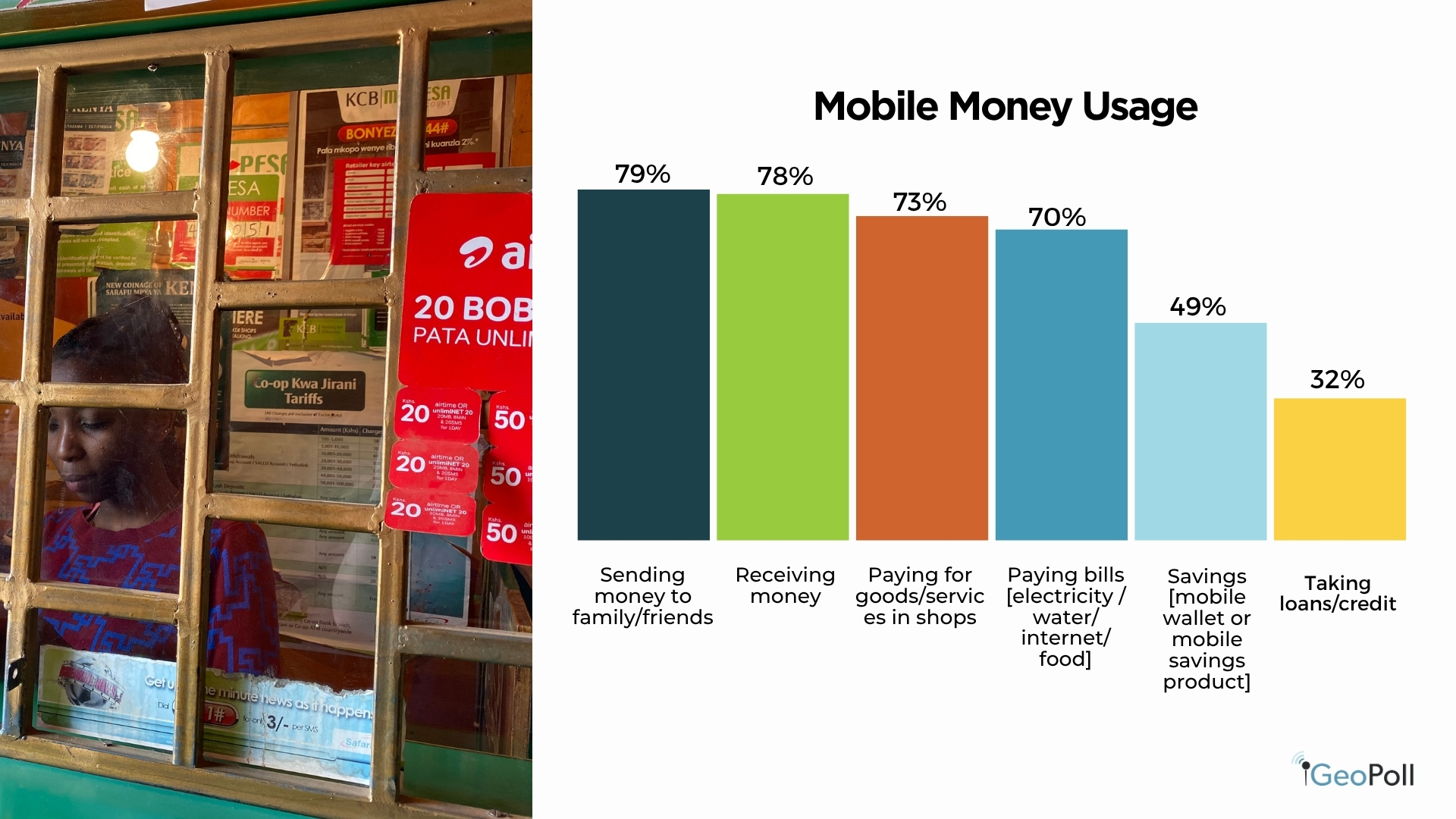

When requested about their foremost makes use of of cellular cash, Kenyans demonstrated its versatility past easy transfers. The bulk use it for sending (79%) and receiving cash (78%), adopted intently by paying for items and companies (73%) and settling payments (70%) similar to electrical energy, water, and web. Moreover, practically half (49%) use cellular cash for financial savings, whereas 32% depend on it for loans or credit score, reflecting the increasing function of digital finance in assembly broader monetary wants. This reveals that cellular cash has advanced from a cost platform right into a multifunctional ecosystem supporting each transactional and monetary administration actions.

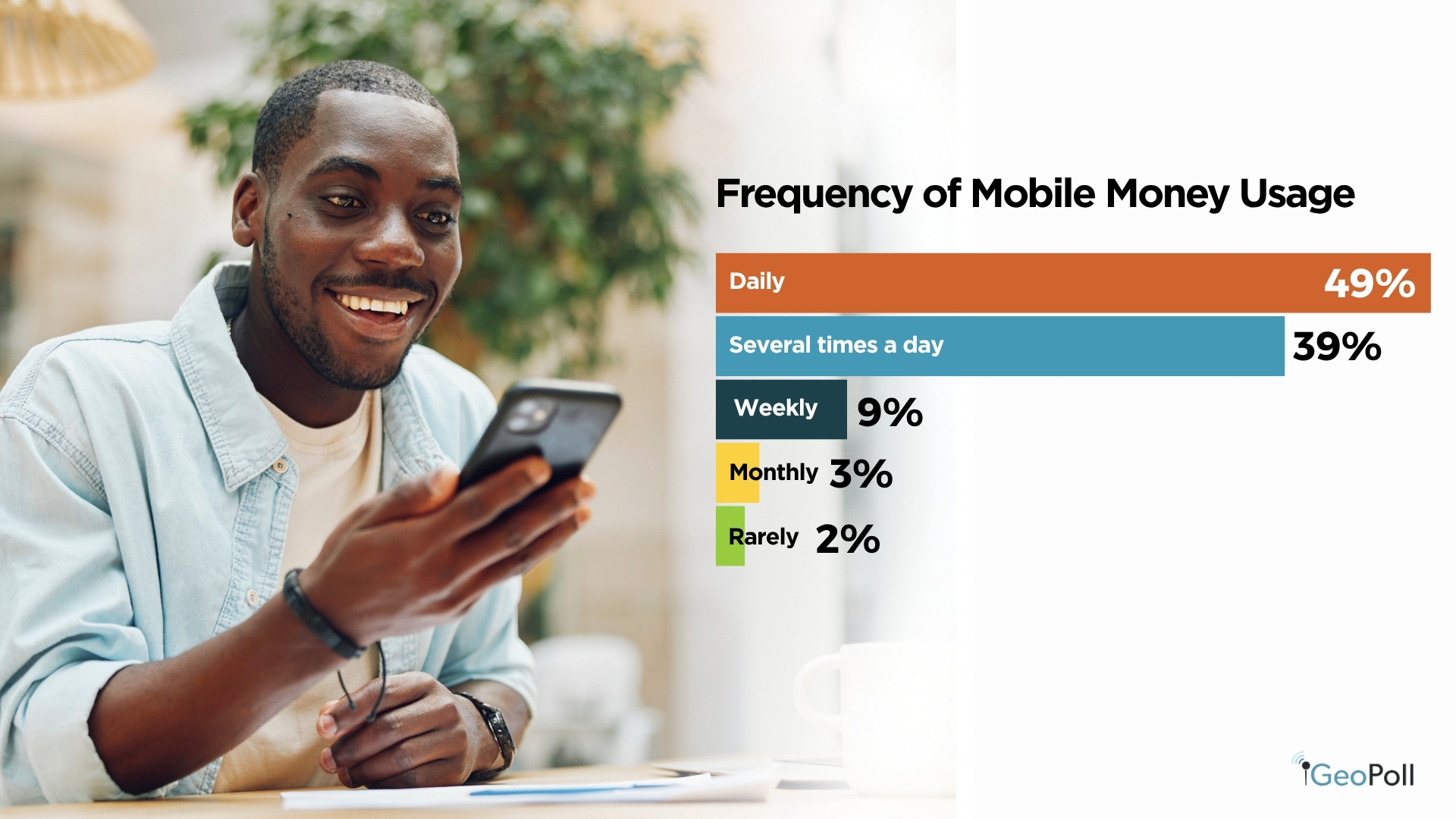

When it comes to frequency of use, engagement is remarkably excessive, 49% of respondents use cellular cash every day, whereas one other 39% transact a number of occasions a day. Solely a small minority use it weekly or much less usually. These patterns show how integral cellular cash has turn out to be to on a regular basis life in Kenya, facilitating every thing from routine purchases to earnings administration. The findings spotlight a mature and extremely lively digital finance atmosphere, the place comfort, belief, and accessibility drive sustained adoption and frequent utilization.

Financial institution Account Possession and Utilization in Kenya

Banking entry in Kenya stays important, although not as widespread or actively used as cellular cash. The findings present that 83% of respondents have a checking account, whereas 17% don’t. Amongst account holders, 40% keep a financial savings account, 23% have a present or checking account, and 21% maintain each sorts. This means that almost all customers prioritize savings-based merchandise, aligning with Kenya’s rising tradition of monetary prudence and long-term planning. Nonetheless, the comparatively excessive share of people with out financial institution accounts highlights the continued significance of other monetary techniques similar to cellular cash and SACCOs.

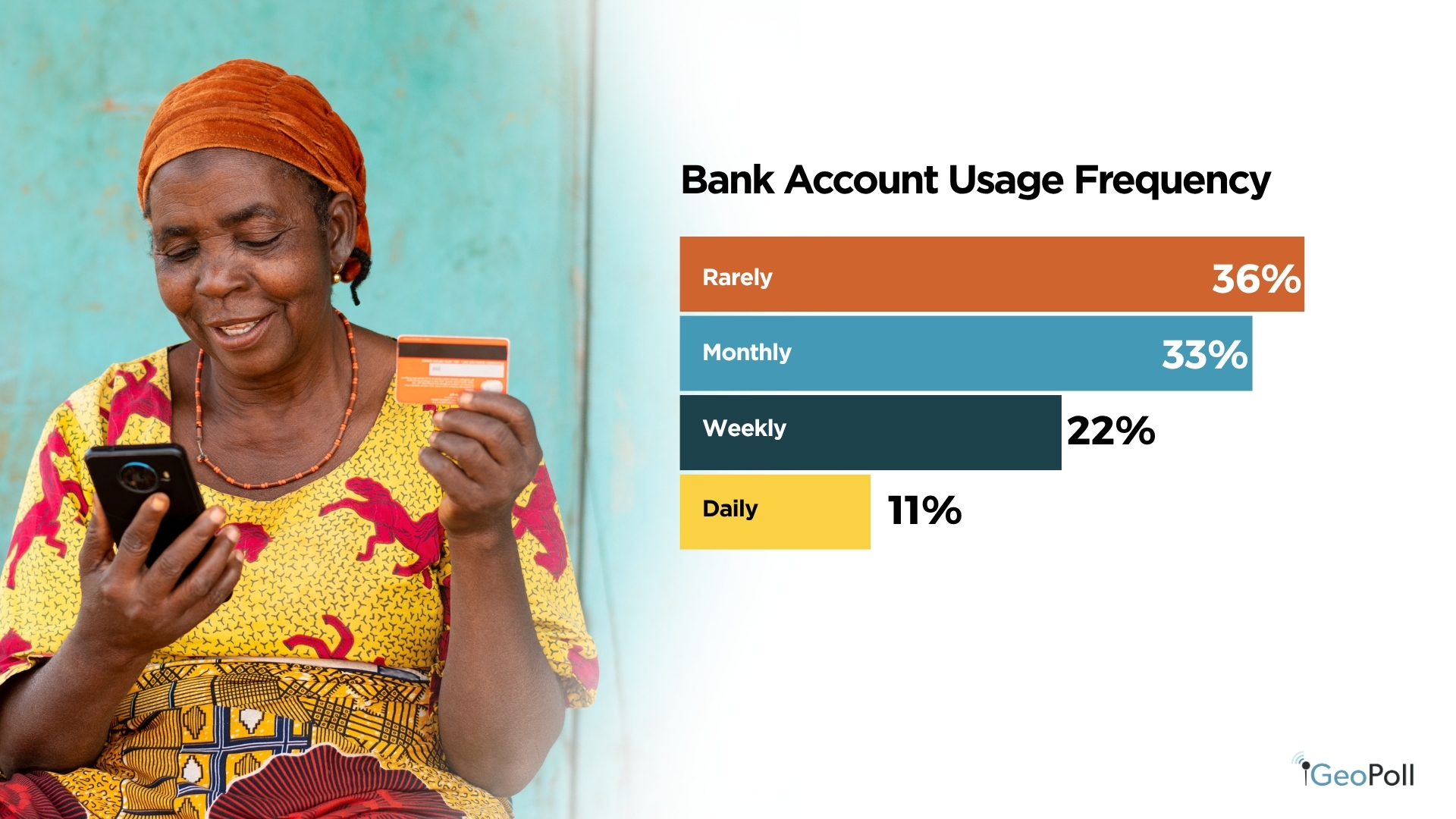

When it comes to frequency of financial institution use, exercise ranges are average to low. About 36% of respondents use their financial institution accounts not often, whereas one other 33% interact with them month-to-month. Solely 22% entry their accounts weekly, and 11% use them every day. This implies that whereas many Kenyans keep formal banking relationships, on a regular basis transactions are much more more likely to happen via cellular platforms, which provide better comfort and accessibility for routine monetary wants.

When requested about their foremost causes for utilizing financial institution accounts, respondents cited receiving earnings (35%) and saving cash (35%) as the highest functions. Smaller proportions reported utilizing banks to pay payments or college charges (8%), conduct enterprise transactions (6%), or entry credit score or loans (4%). These findings present that banks stay trusted for safe deposits and wage dealing with, however are much less built-in into the every day monetary actions that cellular cash now dominates. The info factors to a hybrid monetary atmosphere the place formal banking serves as a basis for financial savings and earnings administration, whereas digital instruments drive on a regular basis monetary interactions.

Prime Banks (% of Mentions)

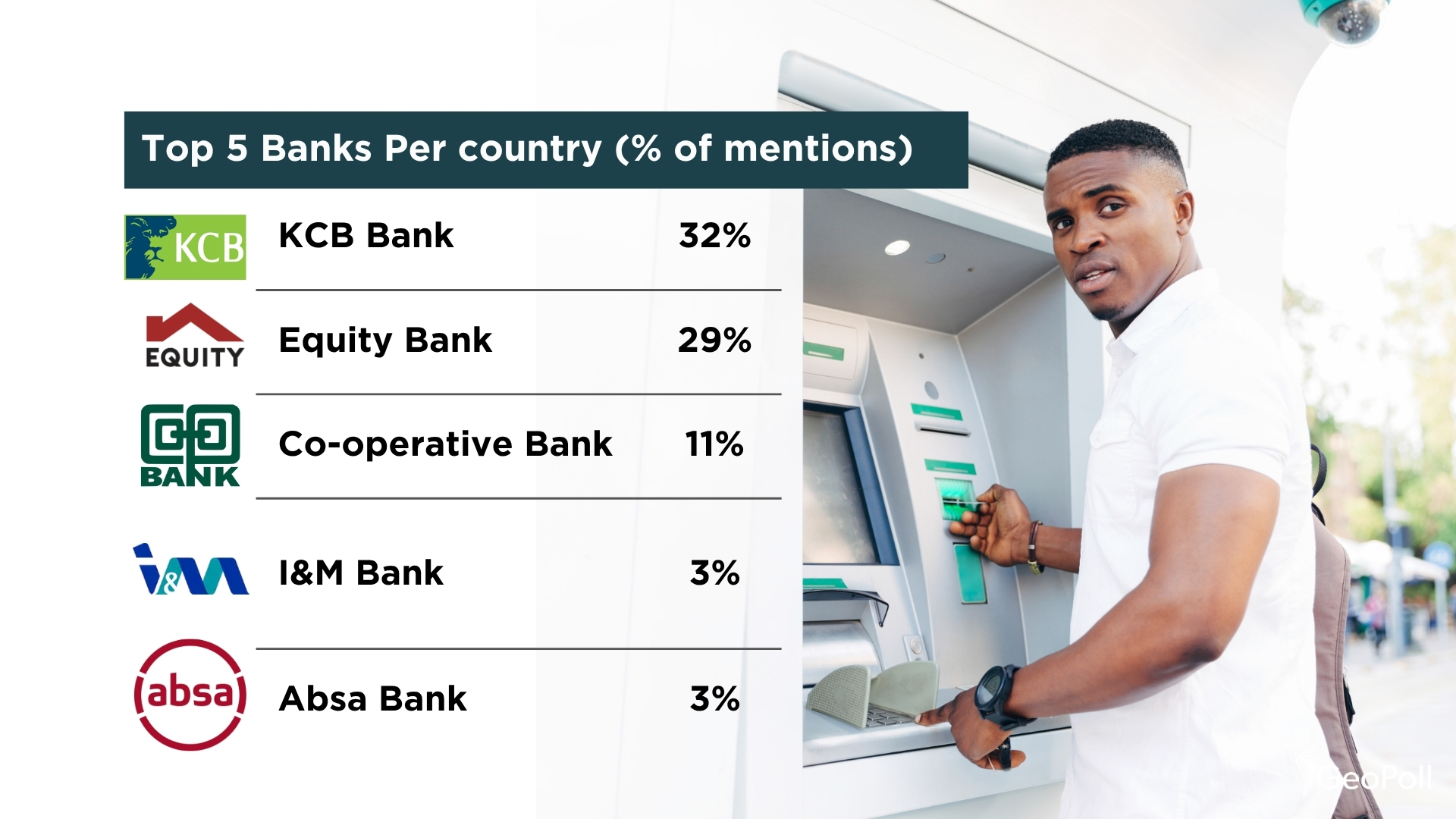

Among the many respondents, the highest 5 most popular banks in Kenya are KCB Financial institution (32%), Fairness Financial institution (29%), Co-operative Financial institution (11%), I&M Financial institution (3%), and Absa Financial institution (3%). The outcomes present a powerful choice for Kenyan-owned establishments, with KCB, Fairness, and Co-operative Financial institution collectively commanding over 70% of respondents. Their dominance highlights the energy of homegrown banks which have constructed intensive networks and deep neighborhood belief, whereas I&M and Absa symbolize smaller however established gamers inside the nation’s diversified banking sector.

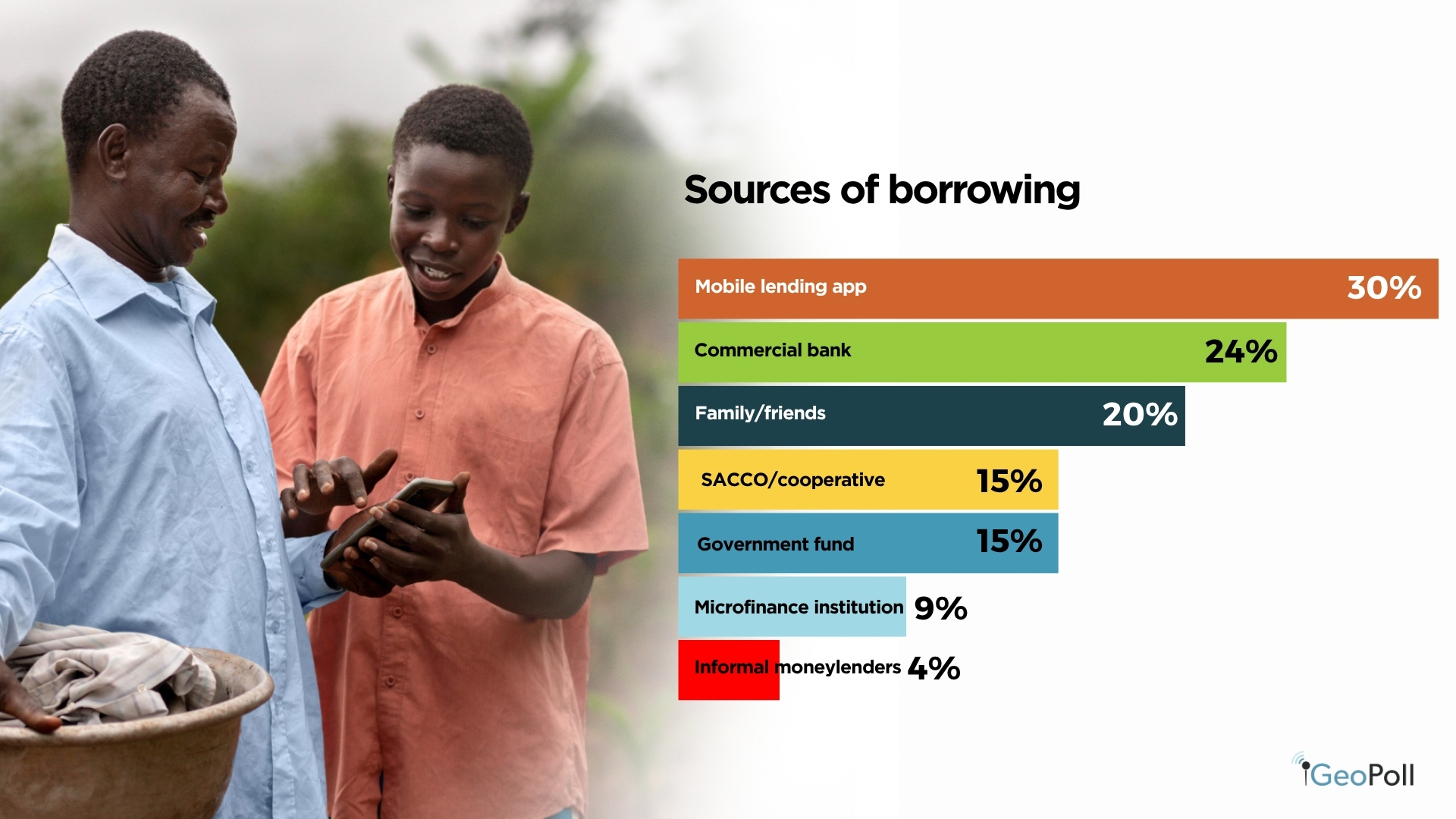

Borrowing Tendencies and Mortgage Sources in Kenya

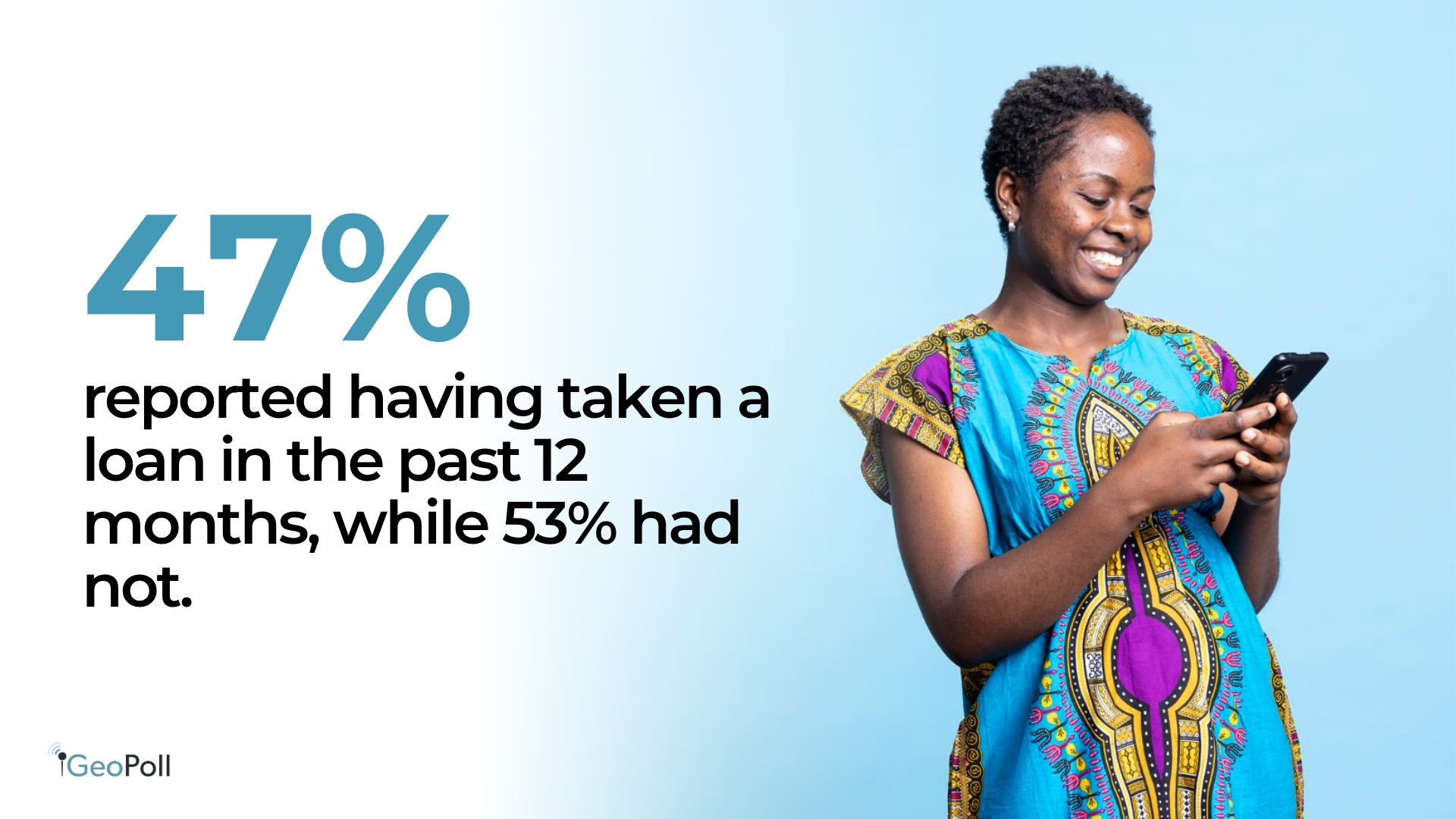

The findings reveal a virtually even break up in borrowing exercise amongst Kenyan respondents. About 47% reported having taken a mortgage up to now 12 months, whereas 53% had not. This steadiness means that credit score entry is comparatively widespread however nonetheless moderated by earnings ranges, monetary literacy, or danger aversion.

When requested about their sources of borrowing, cellular lending apps emerged as the most typical possibility, utilized by 30% of respondents. Their recognition displays the comfort and velocity of digital credit score options like M-Shwari, Tala, and Department. Business banks adopted at 24%, indicating that conventional monetary establishments stay an necessary supply of formal credit score, notably for salaried people. Different notable borrowing sources embody household or pals (20%), SACCOs or cooperatives (15%), and authorities funds (15%), exhibiting a mix of formal and casual mechanisms in Kenya’s credit score panorama. A smaller share borrowed from microfinance establishments (15%) and casual moneylenders (9%), suggesting that whereas entry to credit score is broad, affordability and regulation stay ongoing challenges.

Concerning the principle causes for borrowing, emergencies (27%) topped the listing, adopted by enterprise functions (23%) and faculty or training charges (12%). These patterns spotlight that borrowing in Kenya is essentially pushed by short-term wants and income-support actions, somewhat than asset acquisition or long-term investments. Fewer respondents cited borrowing for meals (7%), family bills (5%), or asset purchases (4%), reinforcing that loans are sometimes used as monetary buffers somewhat than instruments for wealth creation.

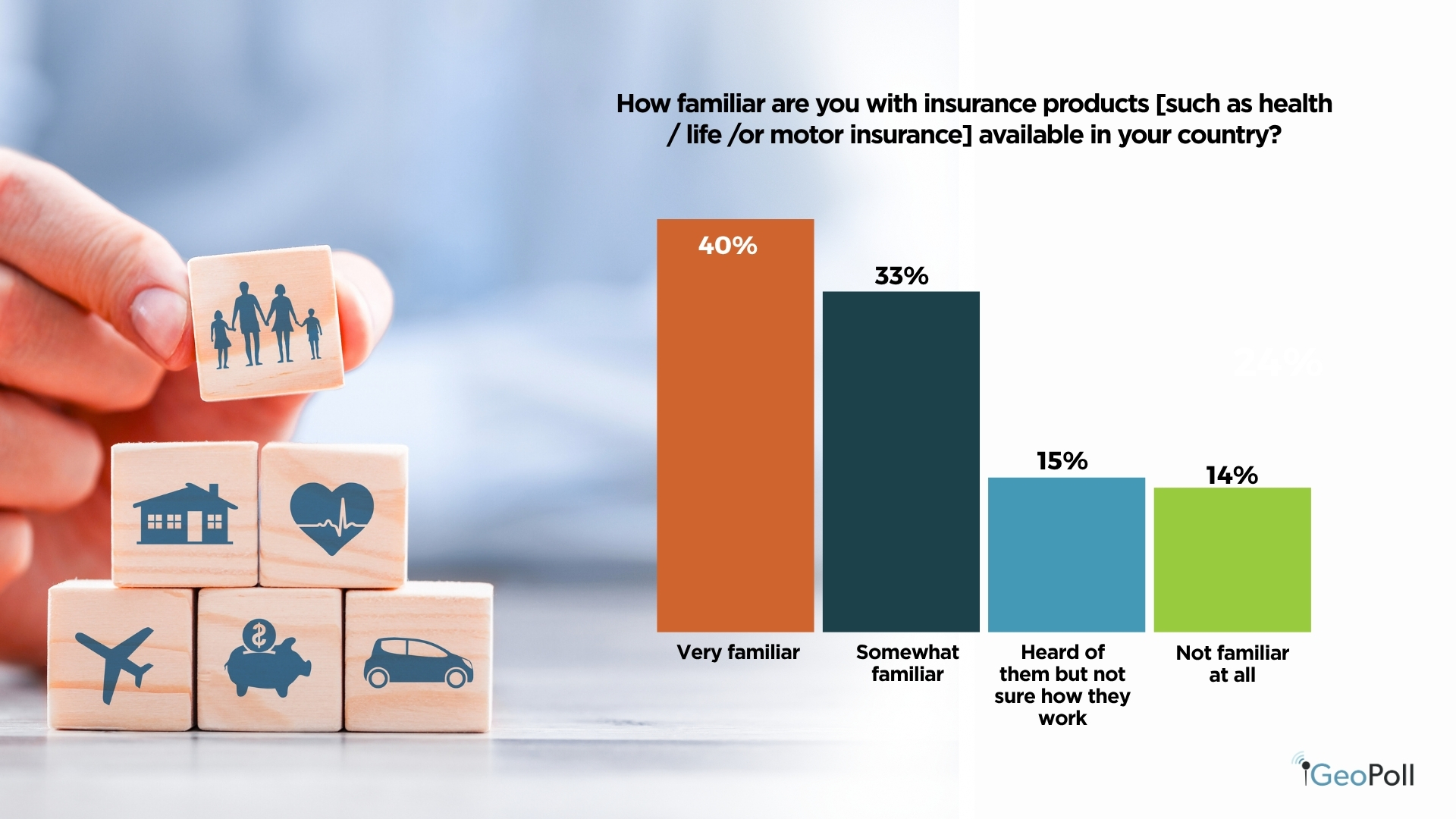

Familiarity with Insurance coverage Merchandise

Most Kenyans show a stable consciousness of insurance coverage, with about 40% saying they’re very aware of totally different insurance coverage merchandise and suppliers. One other 33% are considerably acquainted, exhibiting average understanding. Nonetheless, round 28% have solely heard of insurance coverage or usually are not acquainted in any respect, indicating that whereas consciousness is widespread, deeper understanding stays restricted throughout parts of the inhabitants.

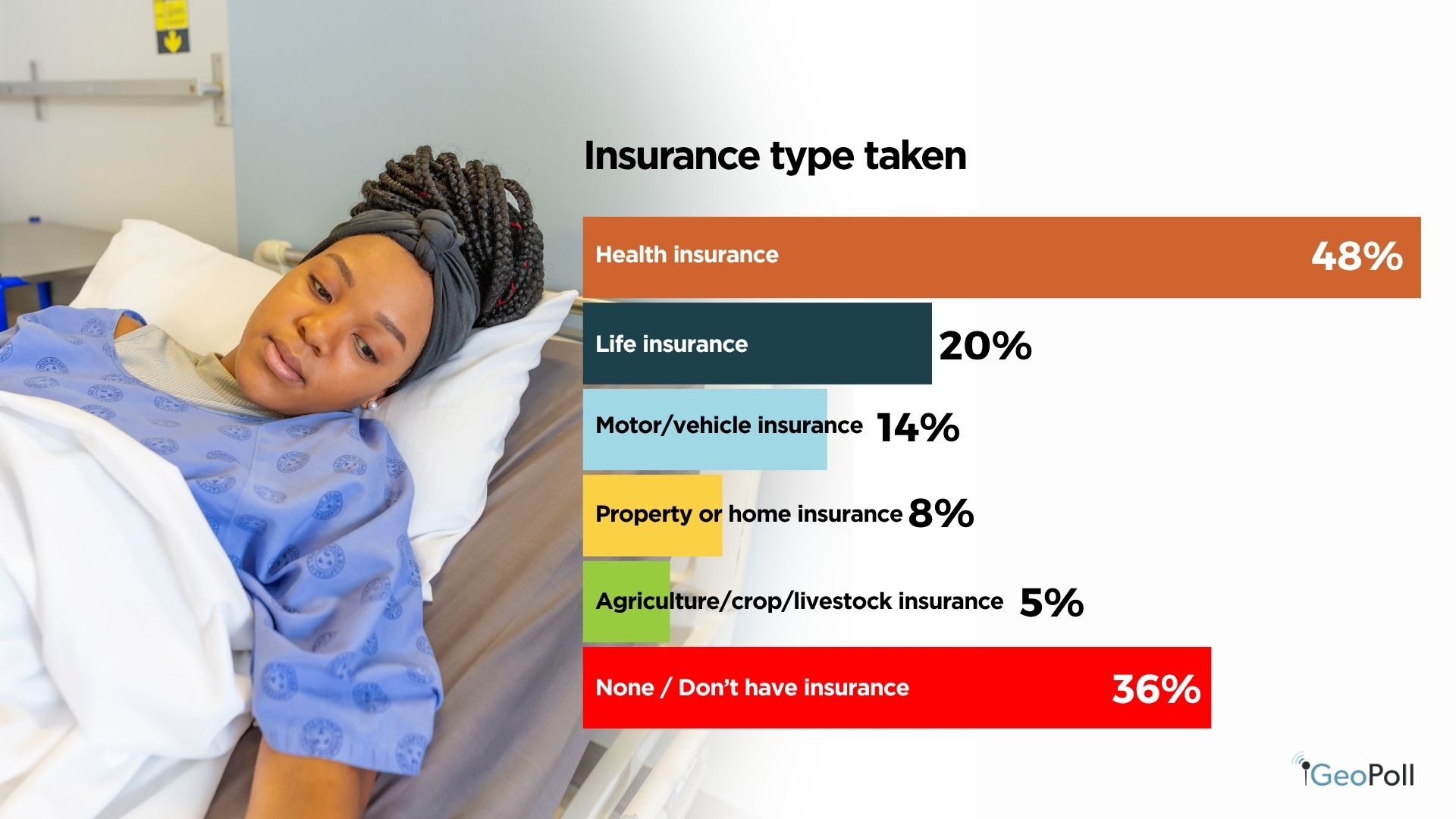

Insurance coverage Uptake and Protection Varieties

Almost half of respondents, 48%, reported having taken an insurance coverage coverage, whereas 53% stated they haven’t. Amongst these insured, medical insurance dominates at 48%, adopted by life insurance coverage at 17% and motor insurance coverage at 14%. Round 36% of respondents at the moment don’t have any insurance coverage protection, revealing important alternative for development in different classes similar to property, agricultural, and residential insurance coverage.

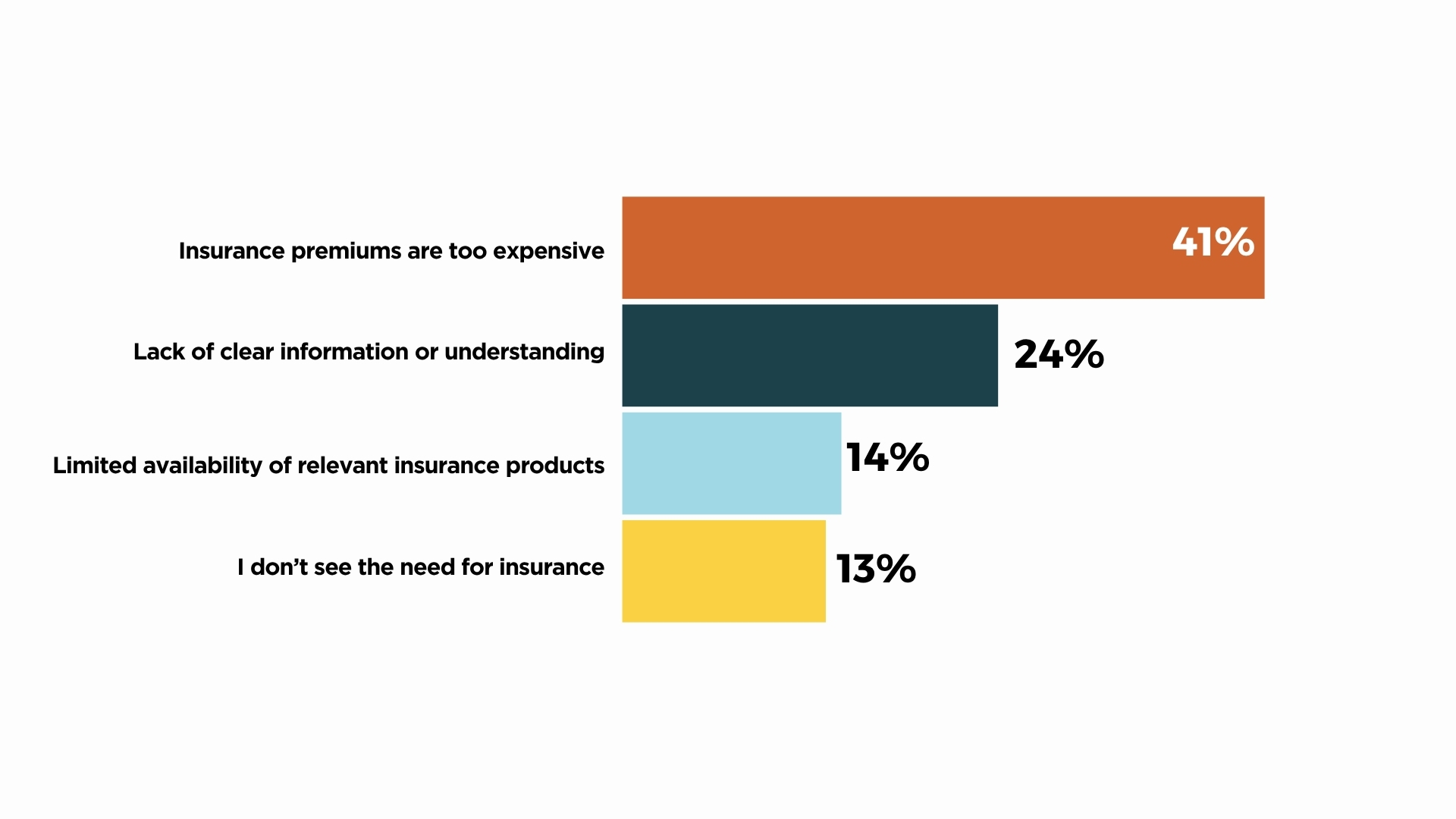

Obstacles to Insurance coverage Uptake

The principle problem limiting insurance coverage adoption is affordability, with about 41% citing excessive premiums as the most important deterrent. One other 24% pointed to lack of clear data or understanding, whereas 14% talked about restricted product availability. Roughly 13% stated they don’t see the necessity for insurance coverage. These findings spotlight the necessity for extra inexpensive, clear, and accessible insurance coverage choices tailor-made to Kenyan customers.

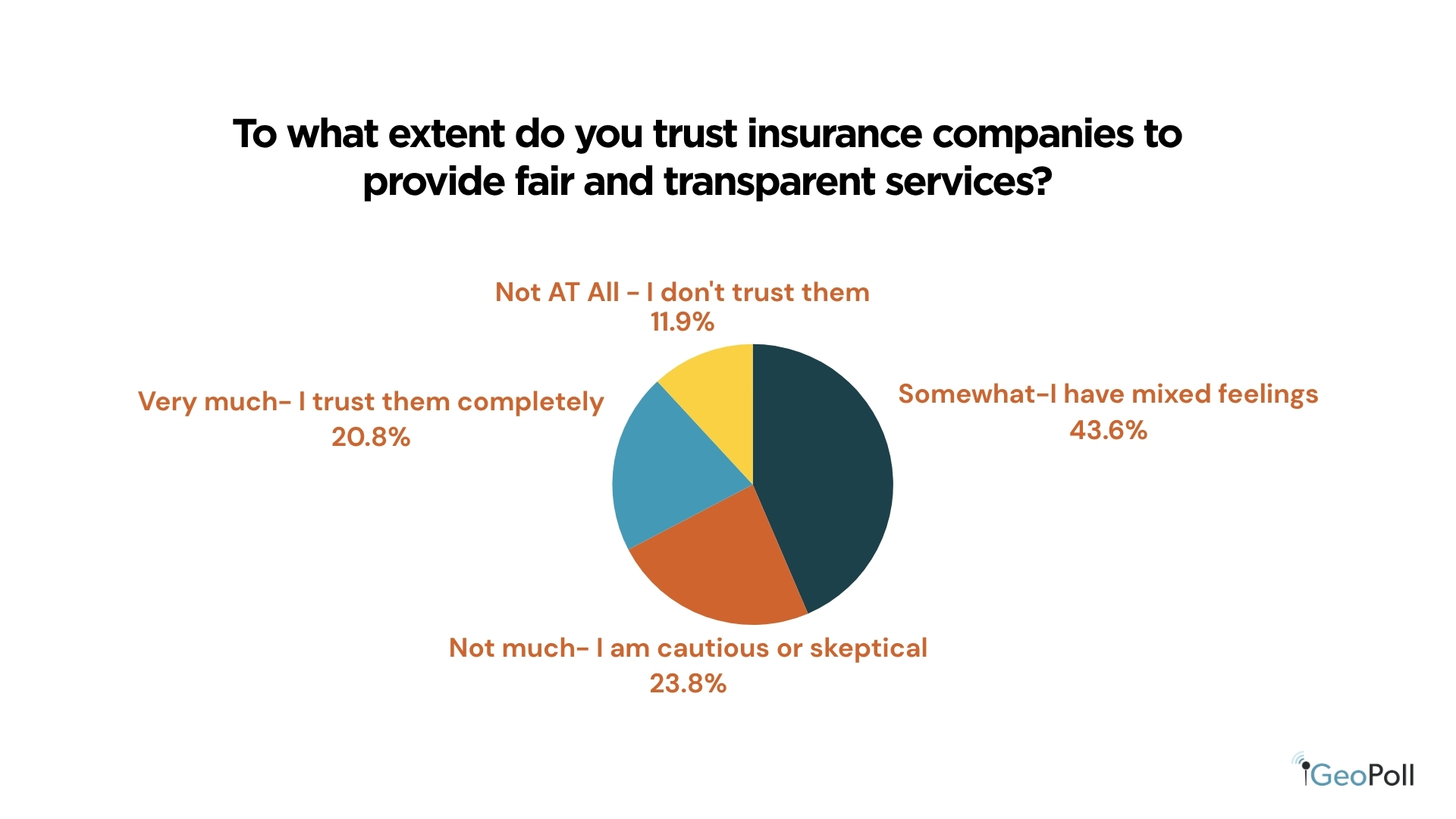

Belief in Insurance coverage Firms

Belief ranges in insurance coverage firms are average. About 44% of Kenyans have combined emotions, 24% are cautious or skeptical, and 21% absolutely belief insurers. Solely 12% say they don’t belief them in any respect. These outcomes present that whereas consciousness is rising, confidence stays restricted, highlighting the necessity for insurers to enhance transparency and construct stronger buyer relationships.

Challenges, Obstacles, and Satisfaction with Monetary Companies

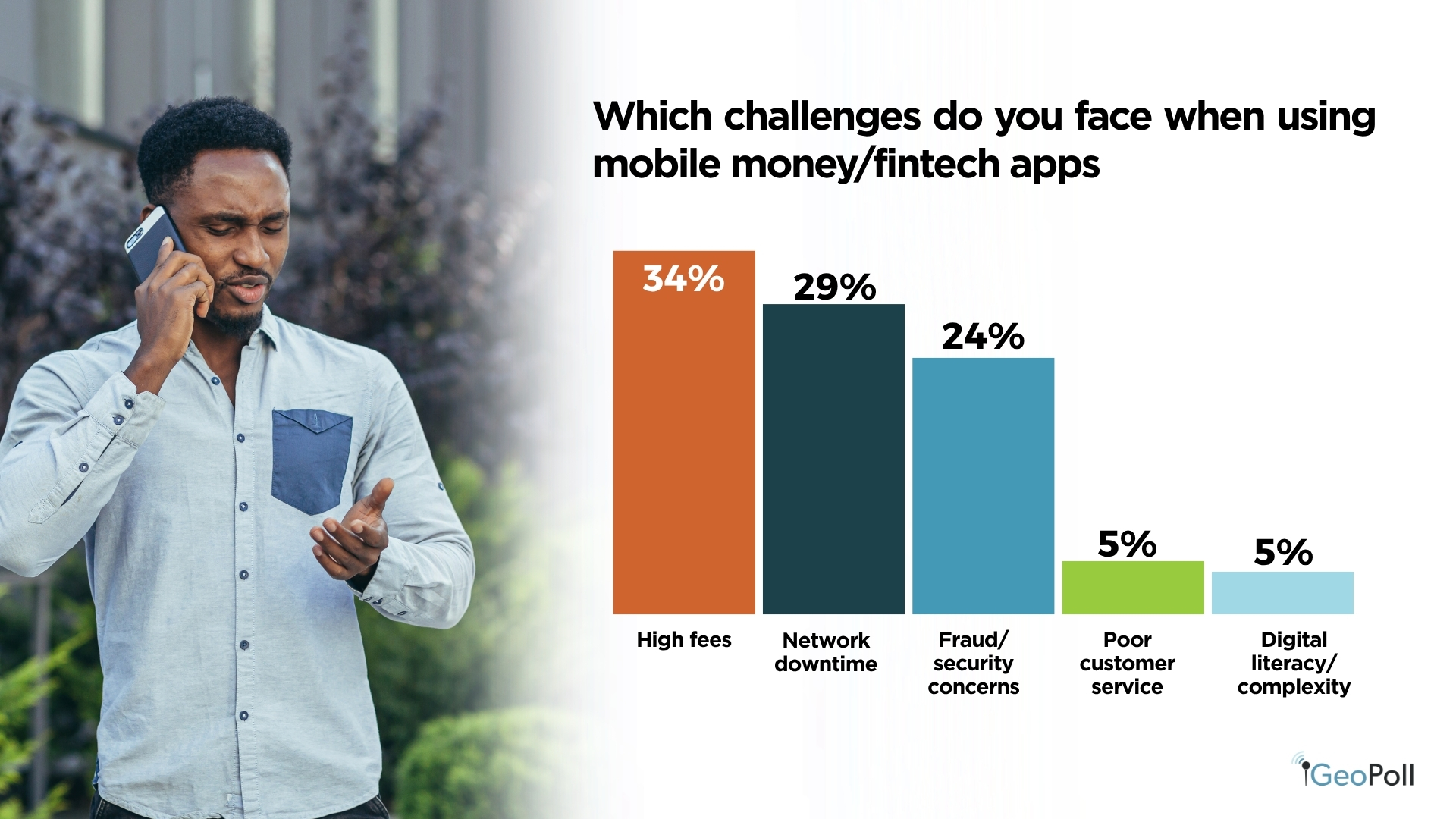

Excessive charges stay a serious concern throughout each cellular cash and formal monetary companies, with 34% of respondents citing them as the principle problem in fintech use and 46% figuring out them as the most important barrier to accessing formal monetary techniques. Different important points embody community downtime at 28% and fraud or safety considerations at 25%, whereas customer support and digital literacy challenges had been reported by fewer customers.

Regardless of these challenges, total satisfaction with monetary companies is pretty constructive. About 41% of respondents reported being happy and 14% very happy, whereas 38% had been impartial. Solely a small proportion, roughly 8%, expressed dissatisfaction. This implies that though prices and repair reliability are key ache factors, most customers acknowledge some stage of satisfaction with obtainable monetary companies.

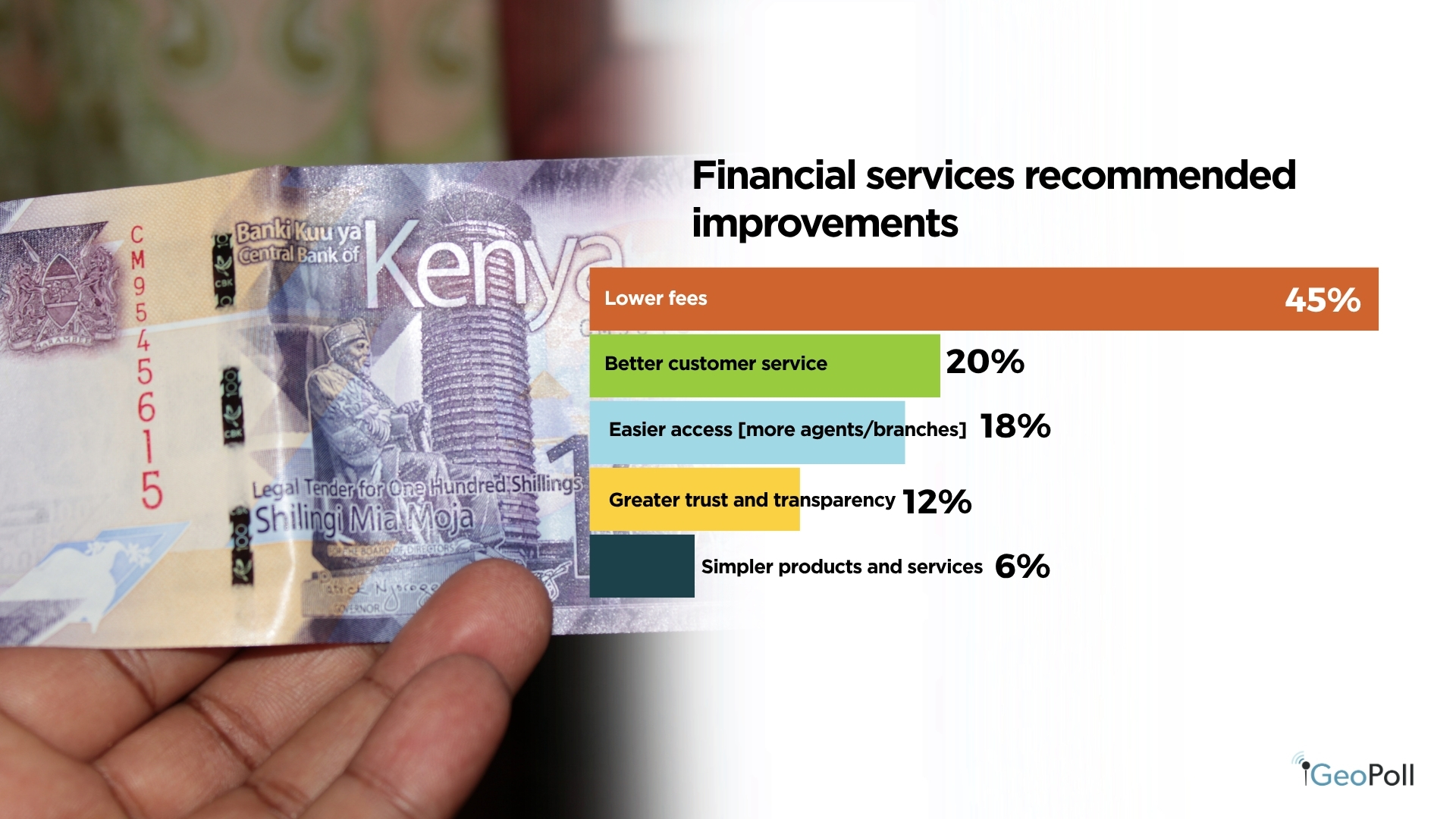

When requested about enhancements that will encourage extra frequent use, practically 45% of respondents known as for decrease charges. Higher customer support and simpler entry to branches or brokers had been additionally seen as necessary by 20% and 19%, respectively. These insights spotlight a transparent demand for affordability, comfort, and improved service supply to reinforce engagement with monetary merchandise in Kenya.

Monetary Constraints and Main Life Choices

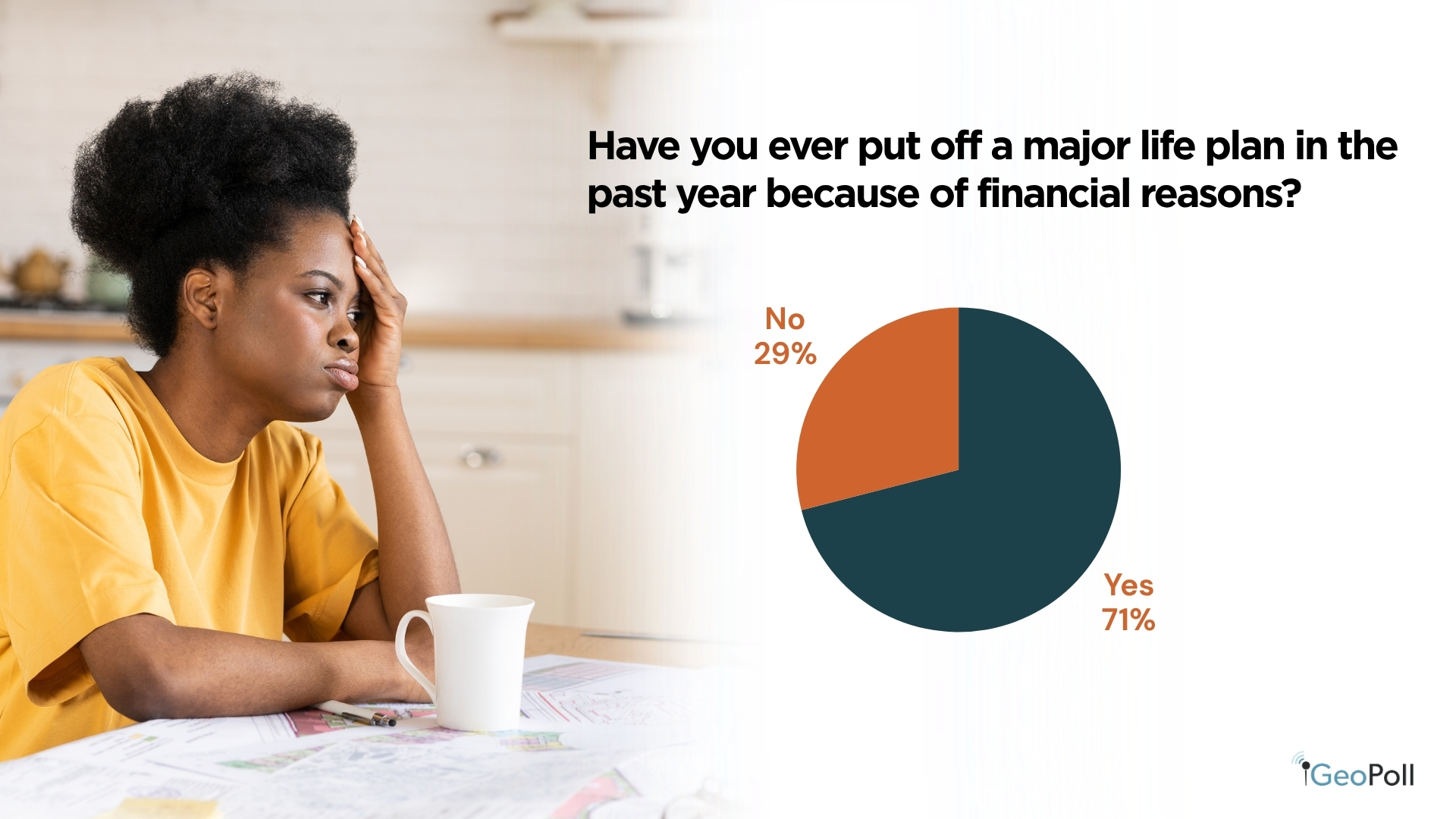

A big majority of respondents, 71%, reported suspending main life plans similar to marriage, training, or beginning a enterprise because of monetary causes. Solely 29% stated they’d not delayed any main plans. This means that monetary challenges stay a major barrier to non-public progress for a lot of Kenyans, affecting long-term targets and total financial well-being.

Client Spending Changes

A major 79% of respondents reported altering a product and choosing a less expensive various, whereas solely 22% stated they’d not. This reveals that almost all Kenyans are making cost-conscious choices, probably influenced by financial pressures and the rising price of residing, as they prioritize affordability over model or high quality preferences.

Conclusion

Kenya’s monetary panorama continues to set the tempo for digital innovation in Africa, but clear gaps stay between entry, affordability, and depth of use. With 84.8% of adults now financially included and cellular cash reaching 98% penetration, Kenya has achieved exceptional progress in increasing entry to monetary instruments. Nonetheless, challenges persist: 41% of respondents cite excessive charges as the principle barrier to insurance coverage and monetary service uptake, whereas 44% categorical solely average belief in insurance coverage suppliers.

Monetary pressure stays widespread, with 71% of Kenyans delaying main life choices because of cash constraints and 79% choosing cheaper merchandise to deal with rising prices. Regardless of these pressures, 55% of customers report being happy or very happy with obtainable monetary companies, proof of a inhabitants that continues to be resilient, adaptive, and optimistic. Transferring ahead, Kenya’s monetary ecosystem should prioritize affordability, transparency, and accountable innovation to make sure that its digital success story interprets into sustainable monetary well-being for all.

Methodology/About this Survey

This Unique Survey was powered by GeoPoll’s AI platform; Tuucho run by way of the GeoPoll cellular software and Cellular internet in Kenya, the pattern measurement was 2,500, composed of random customers between 18 and 50. Because the survey was randomly distributed to an prosperous viewers the outcomes are barely skewed in the direction of youthful respondents.

These insights spotlight not solely the evolving nature of Kenya’s monetary panorama, but in addition the facility of GeoPoll in uncovering significant, data-driven narratives throughout various populations. Via its strong mobile-based survey expertise and intensive attain throughout rising markets, GeoPoll delivers quick, dependable, and actionable monetary information that helps organizations, policymakers, and researchers perceive client habits, monetary inclusion, and financial traits in actual time. As digital finance continues to rework entry and utilization throughout Africa, GeoPoll stays on the forefront, bridging the hole between folks and insights, and enabling smarter choices via a deeper understanding of monetary realities.

Please get in contact with us to get extra particulars about our capabilities, discover extra on numerous matters in Africa, Asia, and Latin America.

{kind=link}