Revealed on July seventeenth, 2025 by Aristofanis Papadatos

Dynacor Group (DNGDF) has two interesting funding traits:

#1: It’s providing an above-average dividend yield of three.6%, which is triple the common dividend yield of the S&P 500.

#2: It pays dividends month-to-month as a substitute of quarterly.

Associated: Record of month-to-month dividend shares

You possibly can obtain our full Excel spreadsheet of all month-to-month dividend shares (together with metrics that matter like dividend yields and payout ratios) by clicking on the hyperlink under:

The mix of an above-average dividend yield and a month-to-month dividend makes Dynacor a pretty possibility for particular person buyers.

However there’s extra to the corporate than simply these components. Maintain studying this text to study extra about Dynacor.

Enterprise Overview

Dynacor is an industrial gold processor with core operations in Peru, the place it purchases ore from artisanal and small-scale miners and processes it at its wholly owned Veta Dorada plant in Chala.

The power has a nameplate capability of 430 tons per day and is optimized for steady, high-efficiency throughput. The corporate was based in 1996 and is headquartered in Montreal, Canada.

The enterprise mannequin of Dynacor is exclusive in that it doesn’t have interaction in exploration or mining; as a substitute the corporate operates an intensive ore-purchasing community throughout Peru to supply high-grade feedstock.

Dynacor operates a robust logistics community for accumulating ore, runs its personal labs for evaluation, and handles gold exports with safe, dependable methods. Dynacor additionally reinvests in increasing its provide community and enhancing plant capability, whereas sustaining a lean price construction and constant manufacturing circulation.

Dynacor has drastically benefited from the extremely inflationary atmosphere that has prevailed since 2022. The unprecedented fiscal stimulus packages supplied by most governments in the course of the coronavirus disaster led to a surge of inflation to a 40-year excessive in 2022.

Throughout inflationary intervals, buyers rush to purchase gold, as the valuable steel has all the time offered nice safety towards inflation. Consequently, the worth of gold has practically doubled, from roughly $1,700 in early 2022 to an all-time excessive of $3,330 proper now.

The rally of the worth of gold has been clearly mirrored within the enterprise outcomes of Dynacor. The corporate practically tripled its earnings per share, from $0.11 in 2020 to $0.30 in 2021 and posted all-time excessive earnings per share of $0.46 final 12 months.

Within the first quarter of this 12 months, Dynacor grew its income 18% over the prior 12 months’s quarter, to a brand new all-time excessive of $80.0 million, regardless of a 15% decline in gold gross sales volumes attributable to decrease ore grades. The common promoting value of gold surged 39%, from $2,075 per ounce to $2,878 per ounce, thus simply offsetting the impact of decrease volumes.

Working margin shrank from 13.5% to 11.2% attributable to elevated promoting and administrative bills and earnings per share remained flat at $0.13. For the complete 12 months, we anticipate earnings per share of roughly $0.40.

Progress Prospects

The efficiency of Dynacor over the previous decade displays a slow-building however in the end sharp enchancment in profitability, underpinned by operational self-discipline, plant optimization, and favorable gold market situations.

From 2015 to 2019, earnings per share rose incrementally from $0.09 to $0.13, reflecting sluggish however regular progress as the corporate ramped up the throughput at its Veta Dorada plant and expanded its ore buying community in Peru.

These years noticed operational self-discipline, however earnings progress was restricted by average gold costs and the early-stage scale of the enterprise. Nevertheless, as talked about above, progress of earnings per share has drastically accelerated in the previous few years.

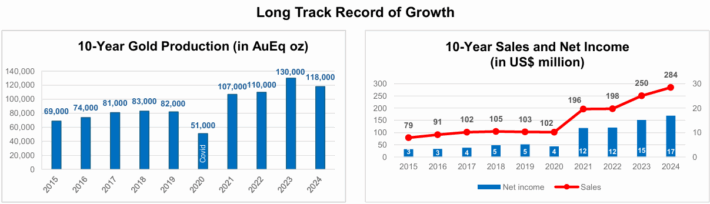

It is usually essential to notice that the corporate has constantly grown its manufacturing over the past decade.

Supply: Reality Sheet

Extra exactly, Dynacor has grown its manufacturing by 6.1% per 12 months on common over the past decade.

We anticipate the corporate to proceed rising its output considerably over the subsequent 5 years. As we additionally anticipate sturdy gold costs to stay in place for the foreseeable future, we anticipate Dynacor to develop its earnings per share at an 8% common annual charge over the subsequent 5 years.

Because of its blowout earnings in recent times, Dynacor has a rock-solid stability sheet. To make sure, it is without doubt one of the only a few corporations that doesn’t pay any curiosity expense, as its curiosity earnings exceeds its curiosity expense. Furthermore, the corporate doesn’t have any debt; as a substitute it has a internet money place of $57 million.

As the web money place is 40% of the market capitalization of the inventory, it’s definitely extreme. General, the rock-solid monetary place of Dynacor is a testomony to the power of its enterprise mannequin.

Dividend & Valuation Evaluation

Dynacor is presently providing an above-average dividend yield of three.6%, which is triple the 1.2% yield of the S&P 500. The inventory is an attention-grabbing candidate for earnings buyers, however they need to remember that the dividend shouldn’t be completely protected as a result of cycles of the worth of gold.

Dynacor has an inexpensive payout ratio of 39%, which offers an honest margin of security for the dividend. Furthermore, due to the promising progress prospects and the pristine stability sheet of the corporate, its dividend ought to be thought of protected within the absence of a serious downturn.

In reference to the valuation, Dynacor is presently buying and selling for 8.3 instances its anticipated earnings per share this 12 months. We assume a good price-to-earnings ratio of 11.0 for this inventory.

Due to this fact, the present earnings a number of is decrease than our assumed honest price-to-earnings ratio. If the inventory trades at its honest valuation degree in 5 years, it can take pleasure in a 5.9% annualized acquire in its returns.

Bearing in mind 8% anticipated progress of earnings per share over the subsequent 5 years, the three.6% present dividend yield and a 5.9% annualized tailwind of valuation degree, Dynacor may provide a 16.9% common annual whole return over the subsequent 5 years. The anticipated whole return signifies that the inventory is very engaging proper now.

Remaining Ideas

Dynacor has promising progress prospects due to manufacturing progress and probably greater gold costs within the upcoming years. The inventory is providing an above-average dividend yield of three.6% and it seems cheaply valued. Consequently, it seems engaging proper now.

Alternatively, the corporate has confirmed extremely susceptible to the cycles of the worth of gold. Consequently, it’s appropriate just for affected person buyers, who can endure excessive inventory value volatility .

Extra Studying

Don’t miss the assets under for extra month-to-month dividend inventory investing analysis.

And see the assets under for extra compelling funding concepts for dividend progress shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to assist@suredividend.com.

")

{kind=link}