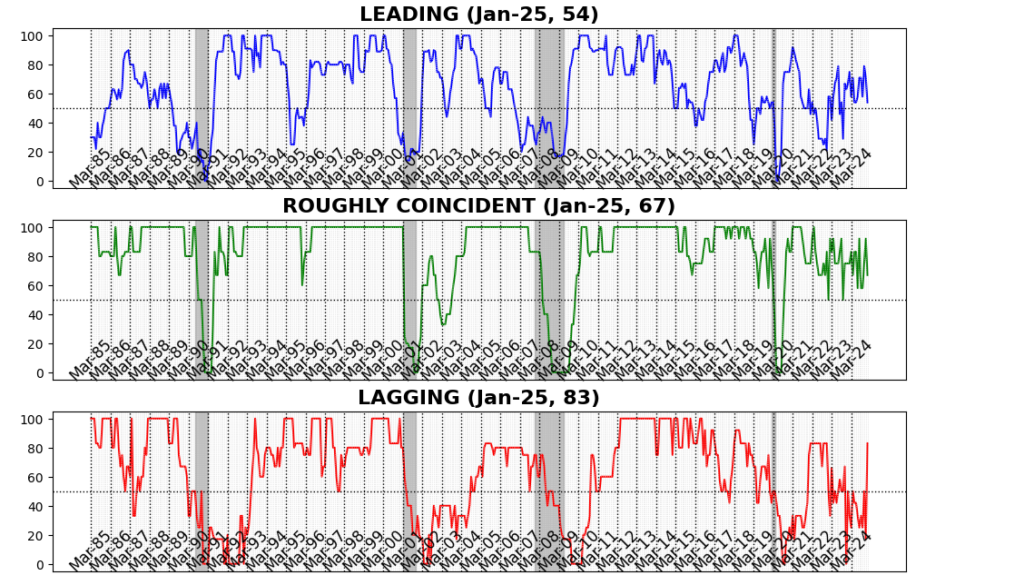

In January 2025, the AIER Enterprise Circumstances Month-to-month indicators confirmed reasonable financial momentum, with main indicators moderating, coincident measures remaining stable, and lagging indicators rebounding sharply. The Main Indicator declined to 54, down from 71 in December, reflecting softening forward-looking financial exercise. Nonetheless, the Roughly Coincident Indicator held agency at 67, indicating regular real-time financial circumstances, whereas the Lagging Indicator surged to 83, suggesting enhancing circumstances in longer-cycle financial tendencies. The divergence between main and lagging measures signifies short-term uncertainty, although the broader economic system reveals resilience for now.

Main Indicator (54)

Of the twelve Main Indicator elements, six rose, one was unchanged, and 5 declined in January.

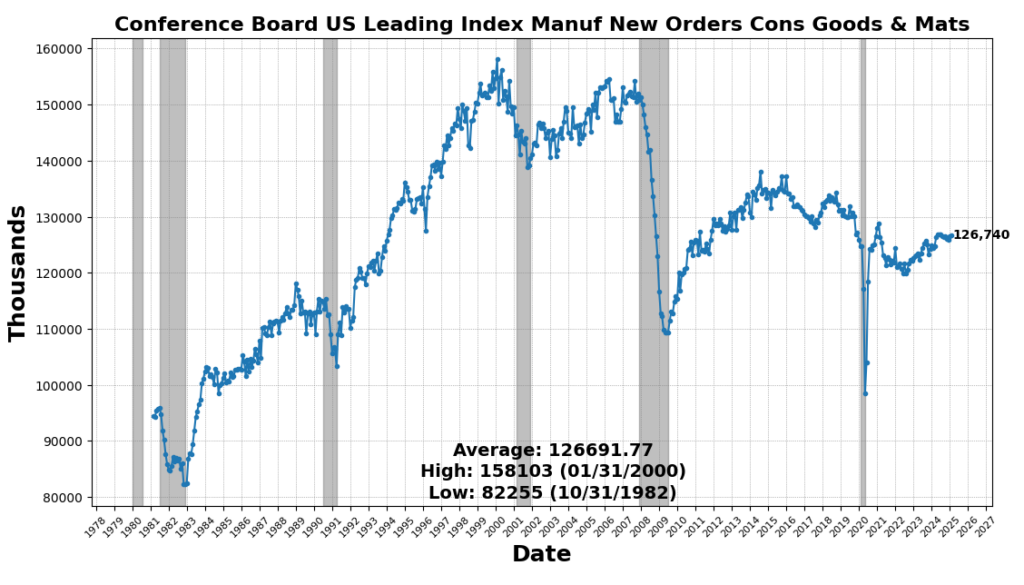

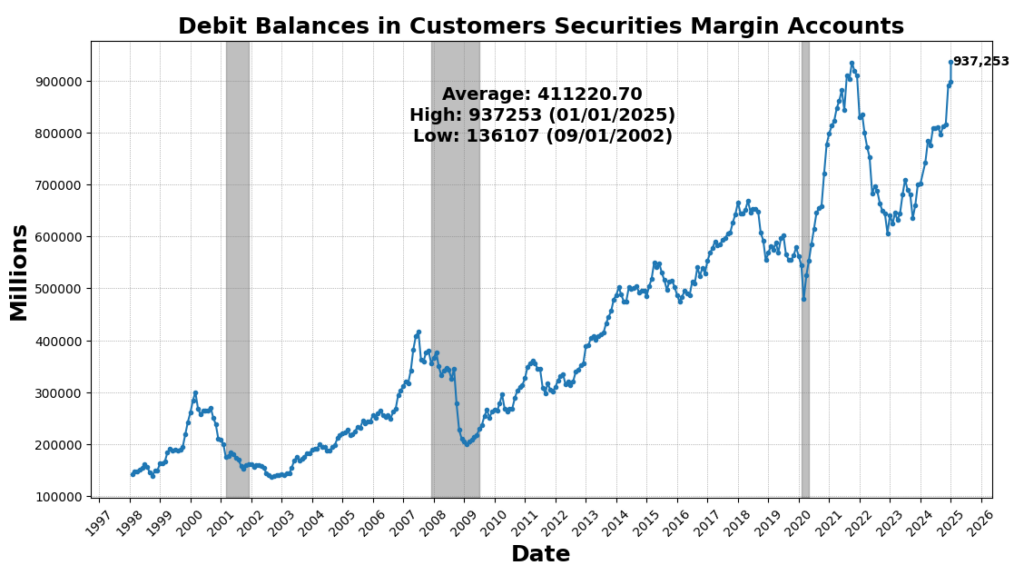

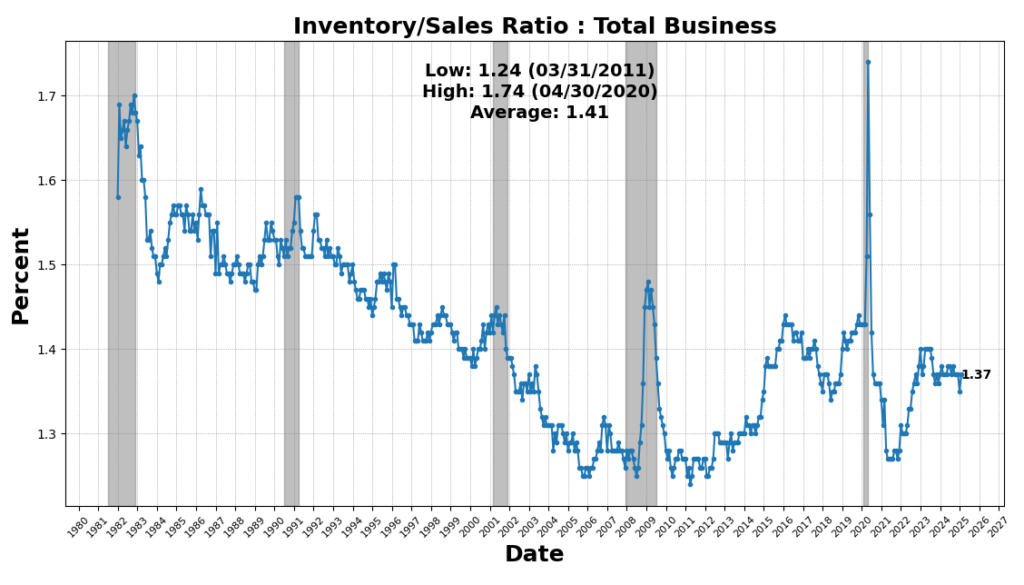

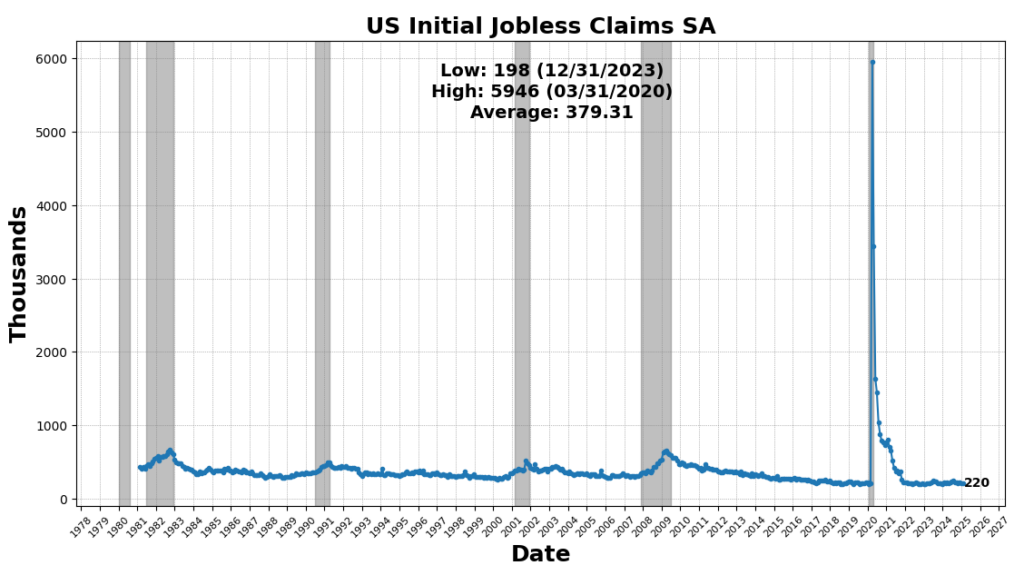

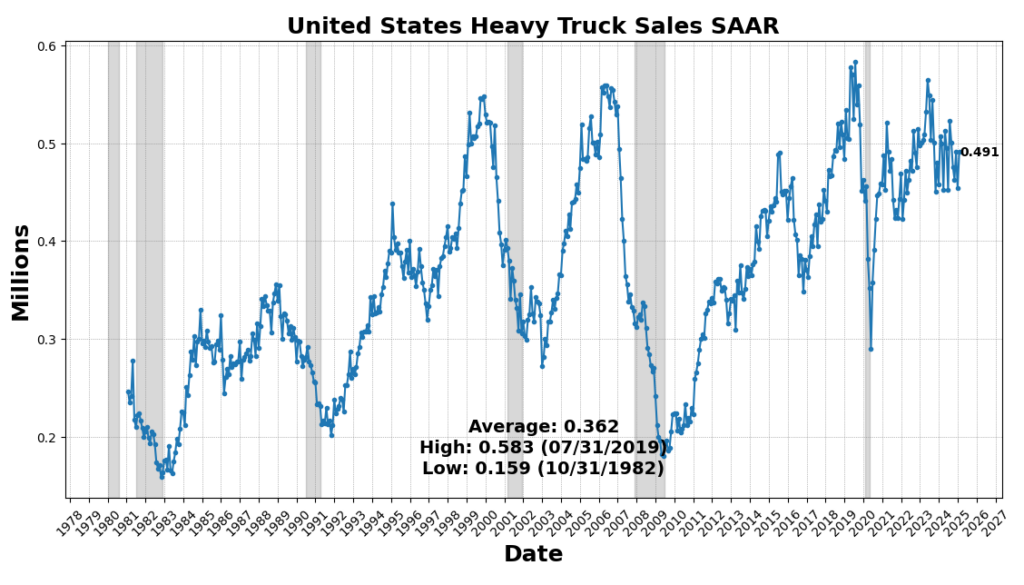

The biggest improve got here from United States Heavy Vehicles Gross sales SAAR, which rose 8.2 %, reflecting continued demand for sturdy items and enterprise funding in transportation gear. Nonetheless, a few of this surge could also be attributed to ahead ordering as companies search to preempt potential price will increase from upcoming tariffs. US Preliminary Jobless Claims SA (4.3 %) and FINRA Buyer Debit Balances in Margin Accounts (4.2 %) additionally elevated, indicating a still-resilient labor market and continued danger urge for food in fairness markets. Manufacturing new orders noticed modest good points, with the Convention Board’s Manufacturing New Orders for Nondefense Capital Items (ex-Plane) up 0.6 % and the Manufacturing New Orders Client Items & Supplies Index up 0.12 %, suggesting marginal power in manufacturing demand. The Stock/Gross sales Ratio rose barely (0.01 %), pointing to flat stock administration tendencies.

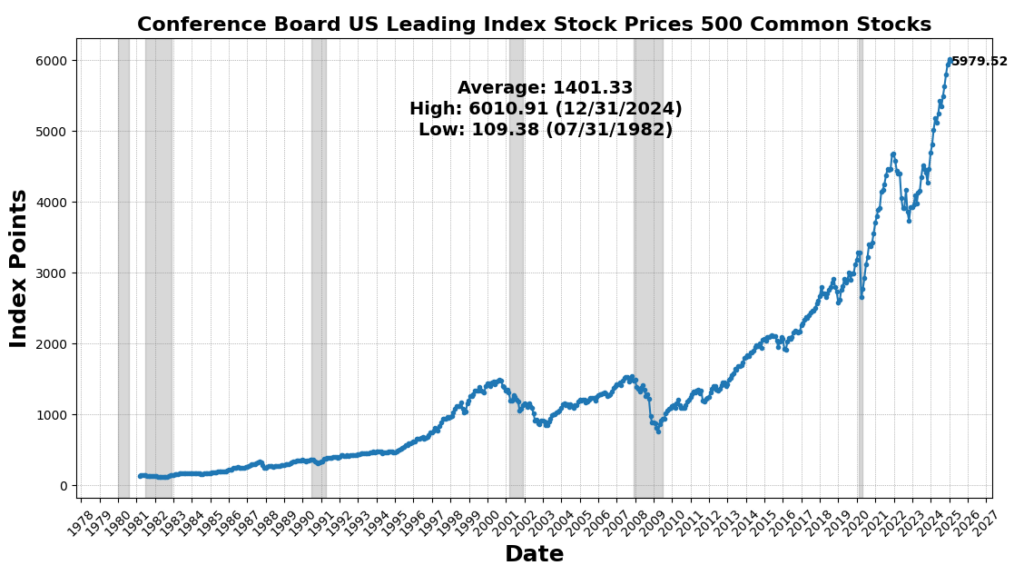

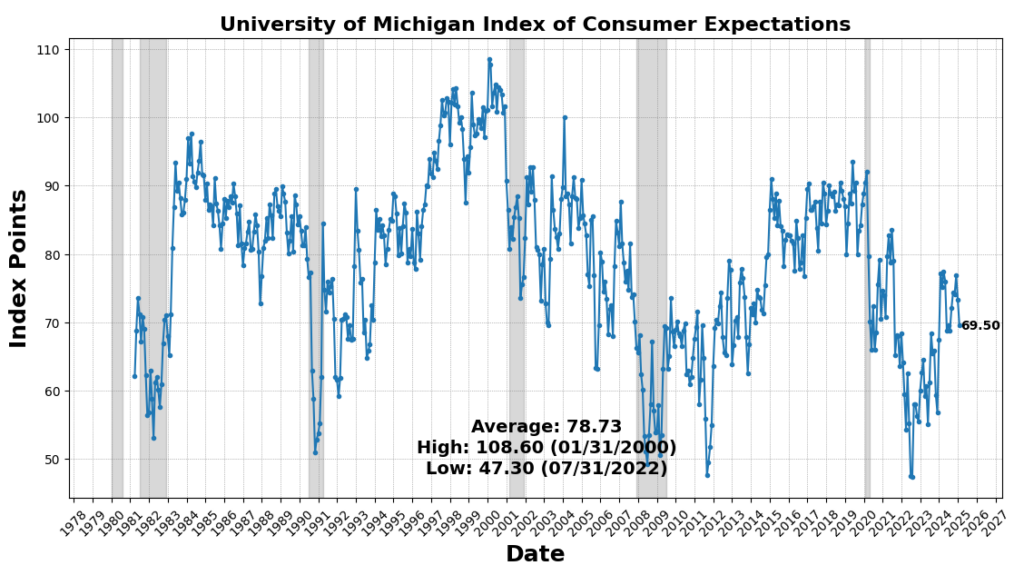

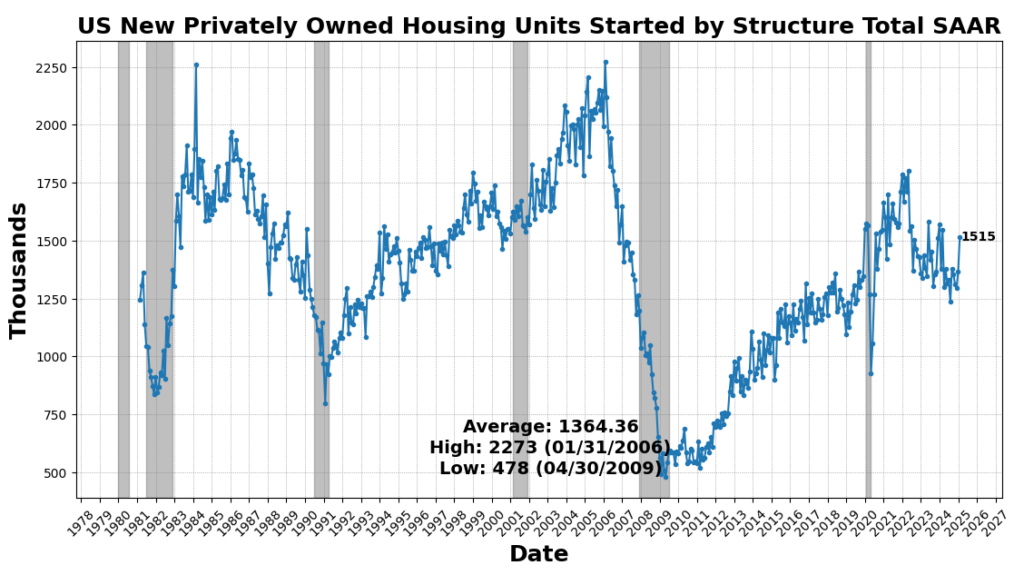

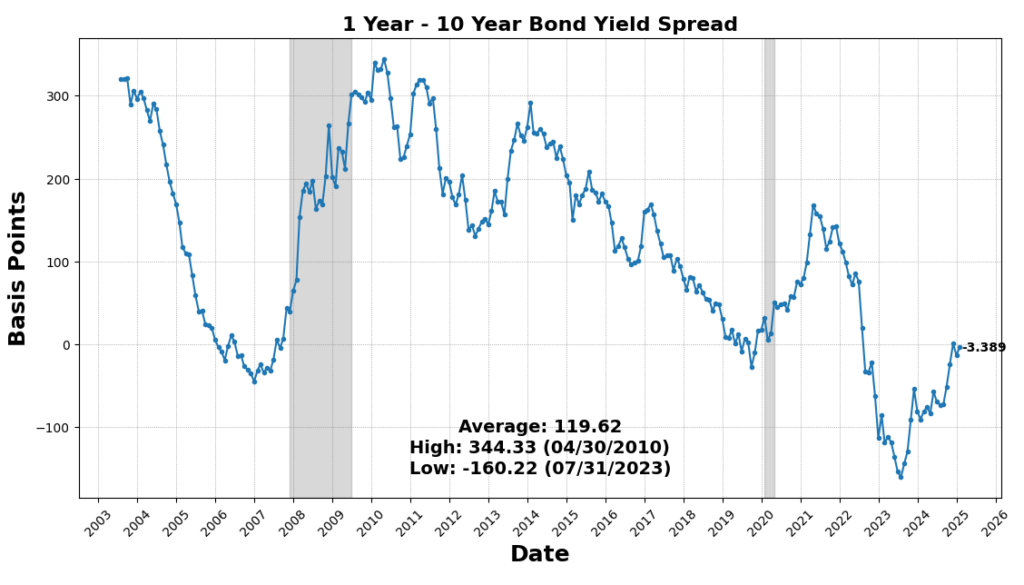

On the draw back, housing exercise remained weak, as US New Privately Owned Housing Models Began fell 9.9 %, marking a continued slowdown in residential development. The 1-to-10 12 months US Treasury unfold declined 8.3 %, sustaining its deep inversion, traditionally a powerful recession sign. Client sentiment weakened, with the College of Michigan Client Expectations Index down 5.3 %, and Adjusted Retail & Meals Providers Gross sales Whole SA down 0.9 %, signaling softening client demand. Lastly, the Convention Board’s Main Index of Inventory Costs fell 0.6 %, reflecting fairness market volatility and investor warning.

Roughly Coincident Indicator (67)

4 constituents of the Roughly Coincident Indicator rose and two declined.

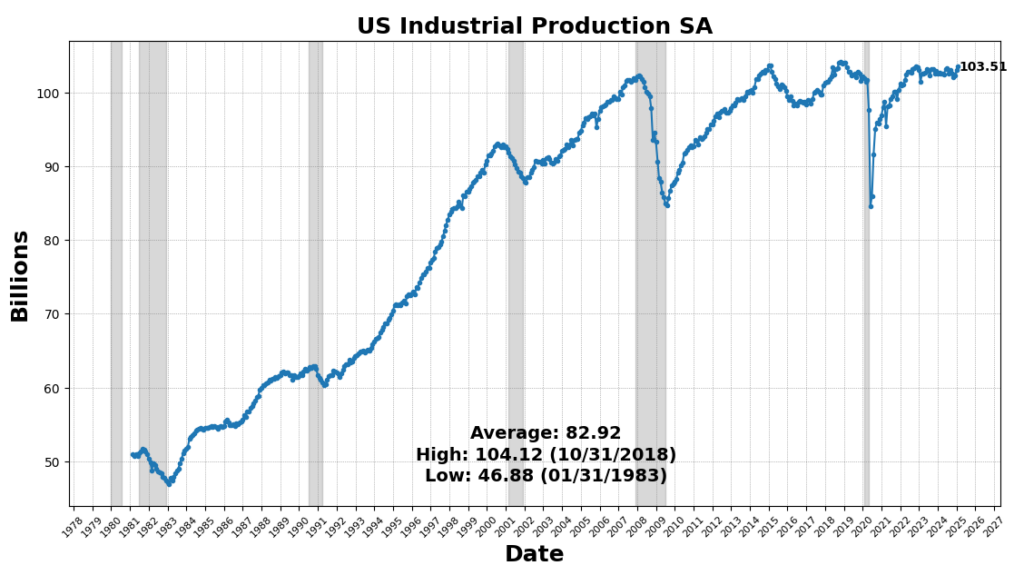

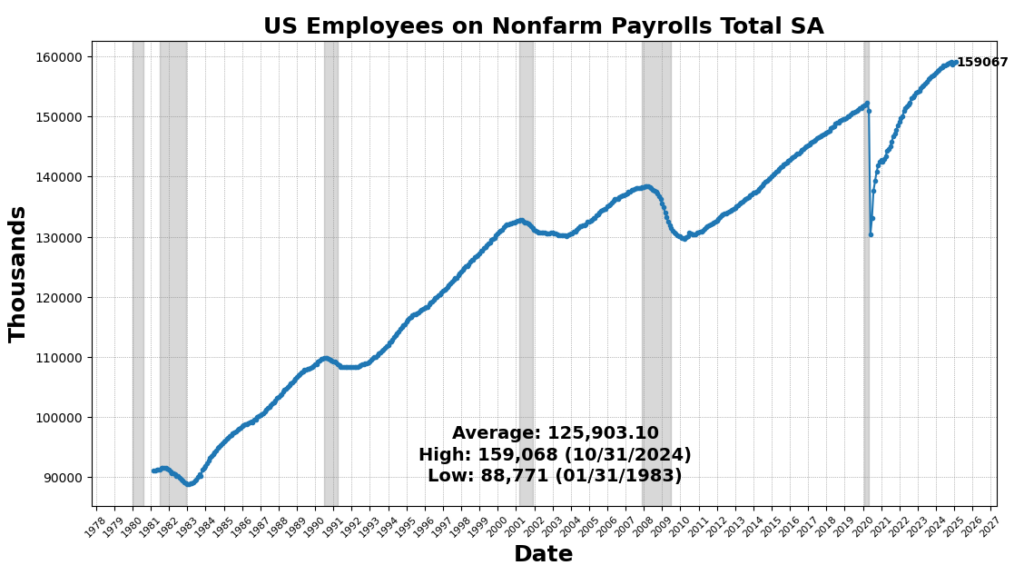

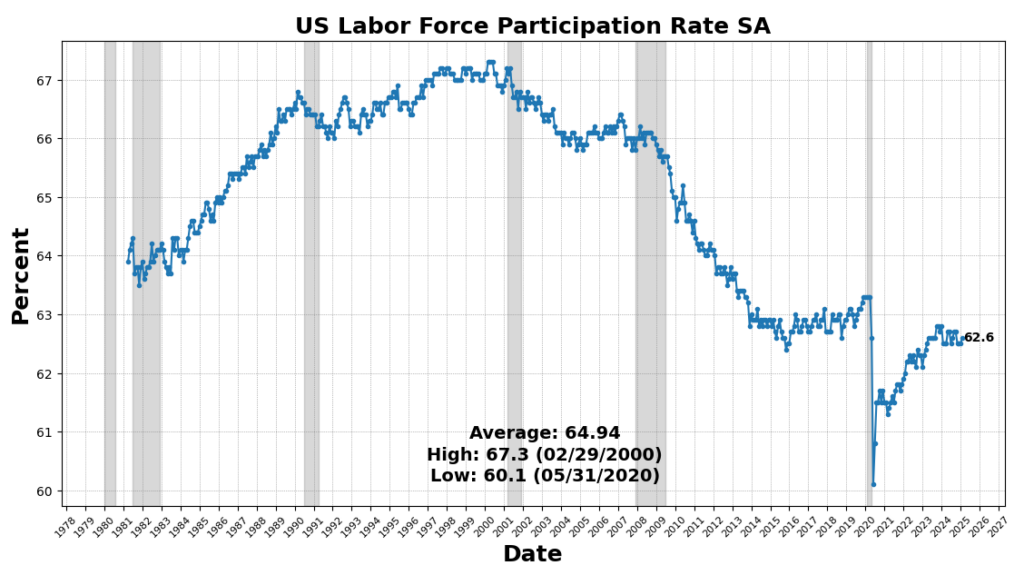

The strongest improve got here from US Industrial Manufacturing SA (0.5 %). Convention Board Coincident Private Revenue Much less Switch Funds rose 0.4 %, indicating reasonable revenue development exterior of presidency assist. Labor market participation improved, with the US Labor Drive Participation Fee up 0.2 % and Nonfarm Payrolls growing barely (0.1 %). These mirror ongoing, however slowing, job development in January 2025.

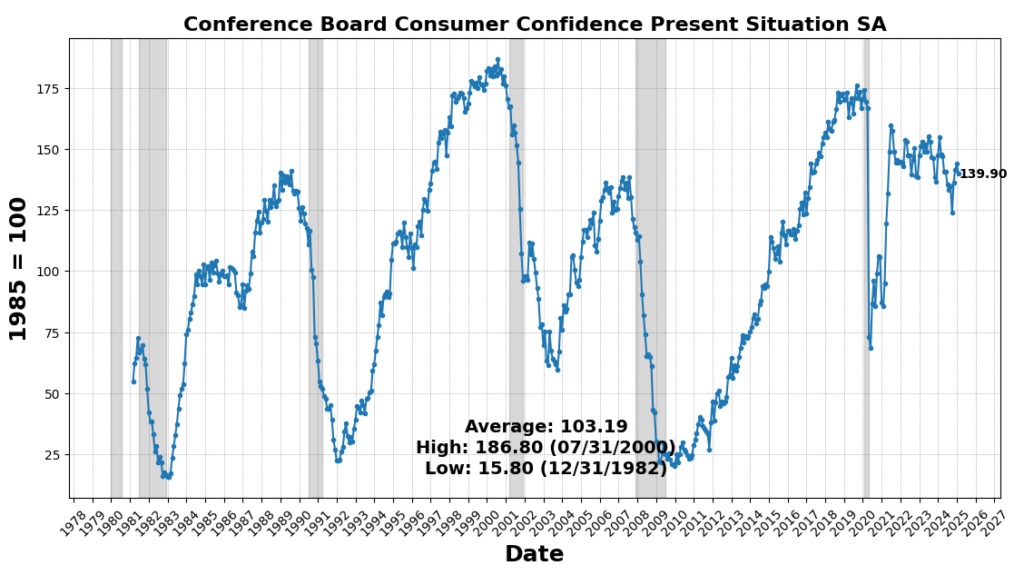

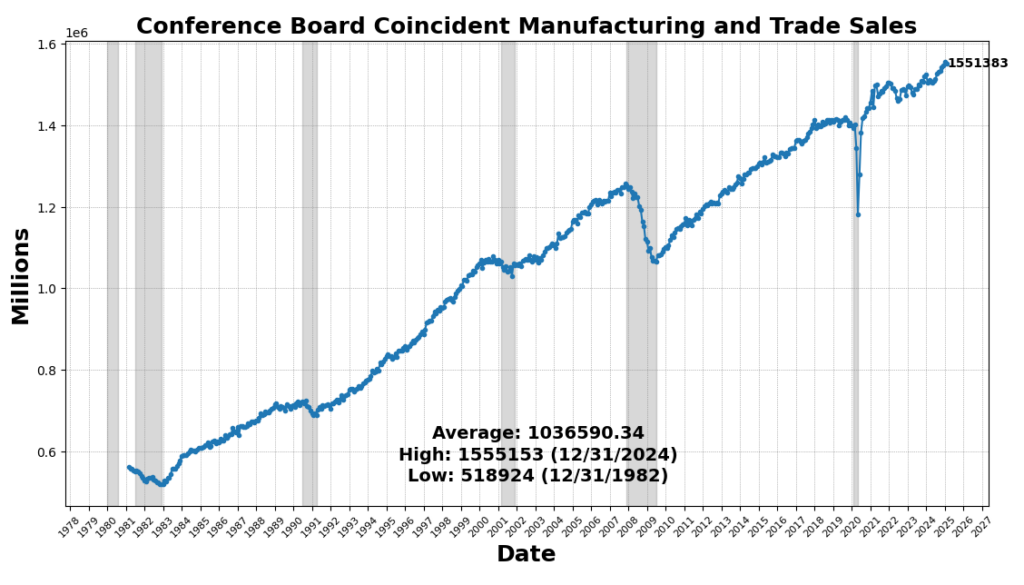

Nonetheless, client sentiment weakened, with the Convention Board’s Client Confidence Current State of affairs Index declining 2.9 %, reflecting rising uncertainty about near-term financial circumstances. Convention Board Coincident Manufacturing and Commerce Gross sales declined barely (0.2 %), suggesting a modest pullback in real-time enterprise exercise.

Lagging Indicator (83)

Of the six elements, 5 rose and one was unchanged. At 83, the Lagging Indicator is at its highest degree in 25 months (December 2022).

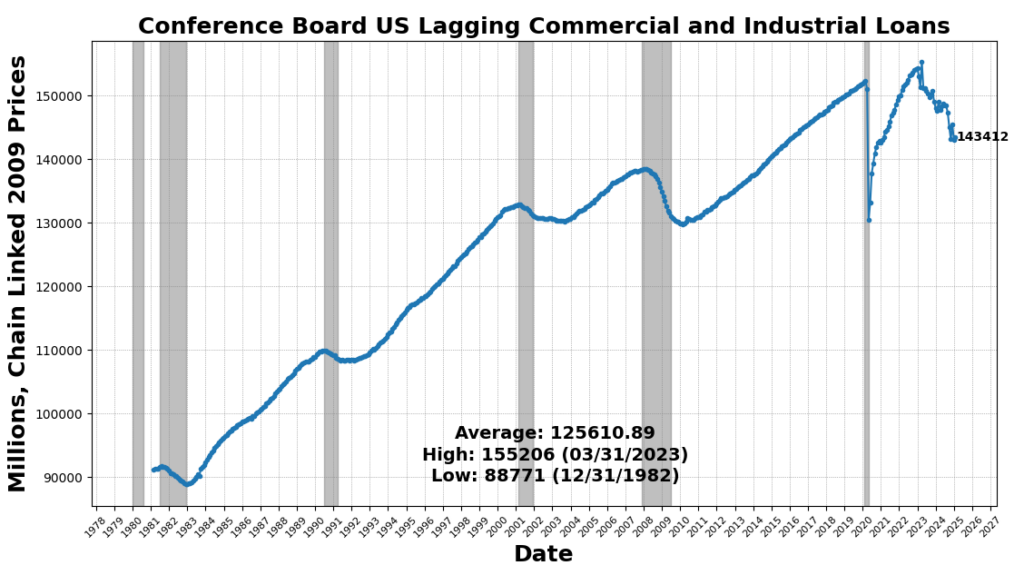

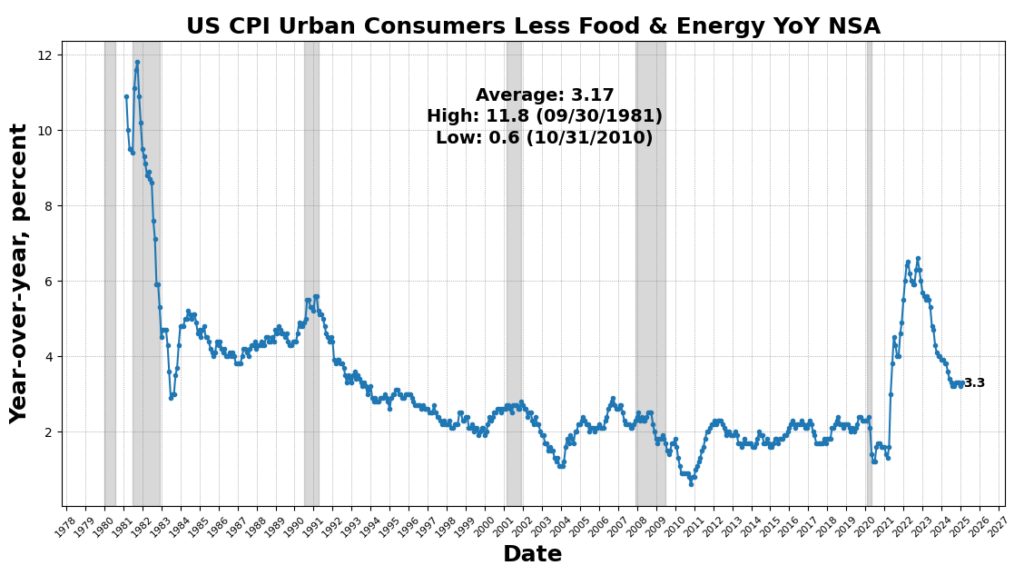

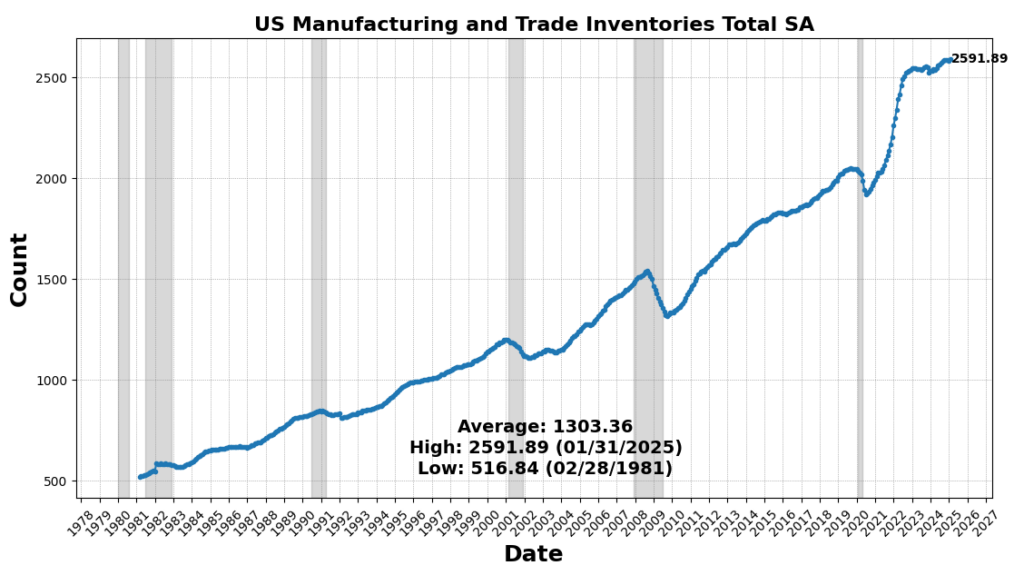

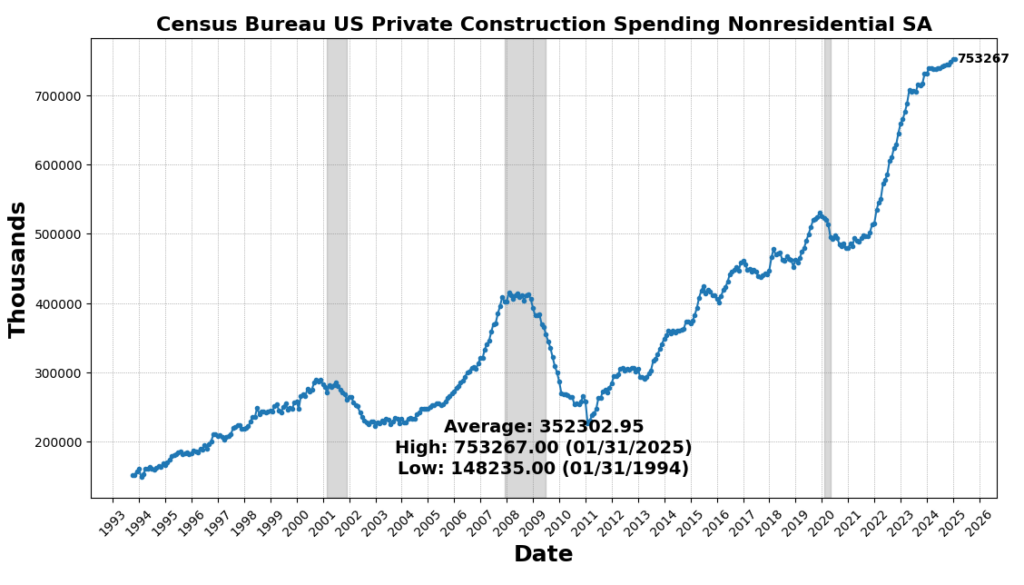

The strongest achieve got here from US CPI City Shoppers Much less Meals & Power YoY (3.1 %), reflecting a slowing of the disinflationary development in core items and companies. Business and Industrial Mortgage exercise improved (0.3 %), and Personal Development Spending noticed a marginal achieve (0.01 %), revealing tepidity in long-cycle enterprise funding. US Manufacturing & Commerce Inventories ticked up very barely (0.003 %), signaling cautious, or maybe hesitant, changes to stock.

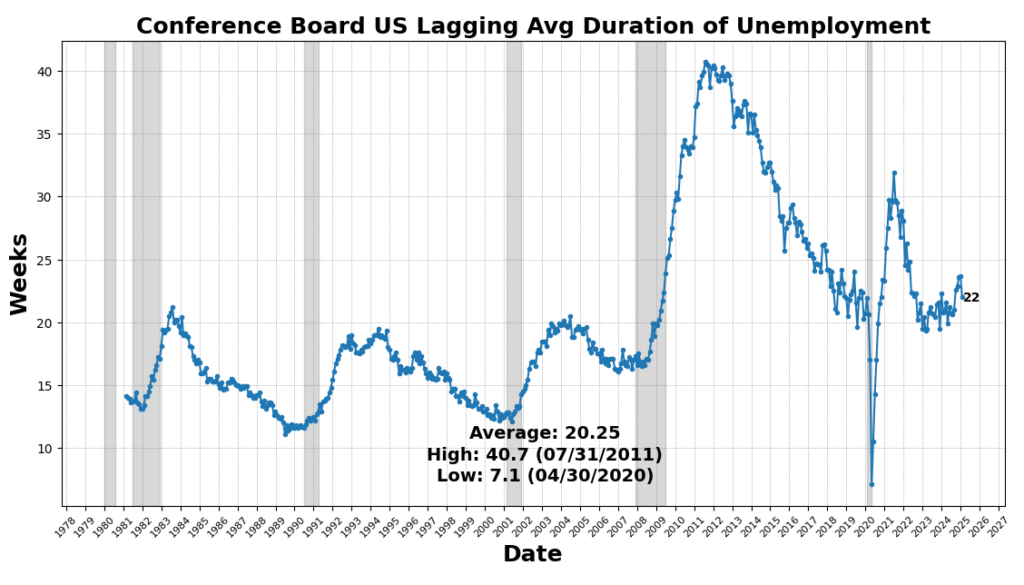

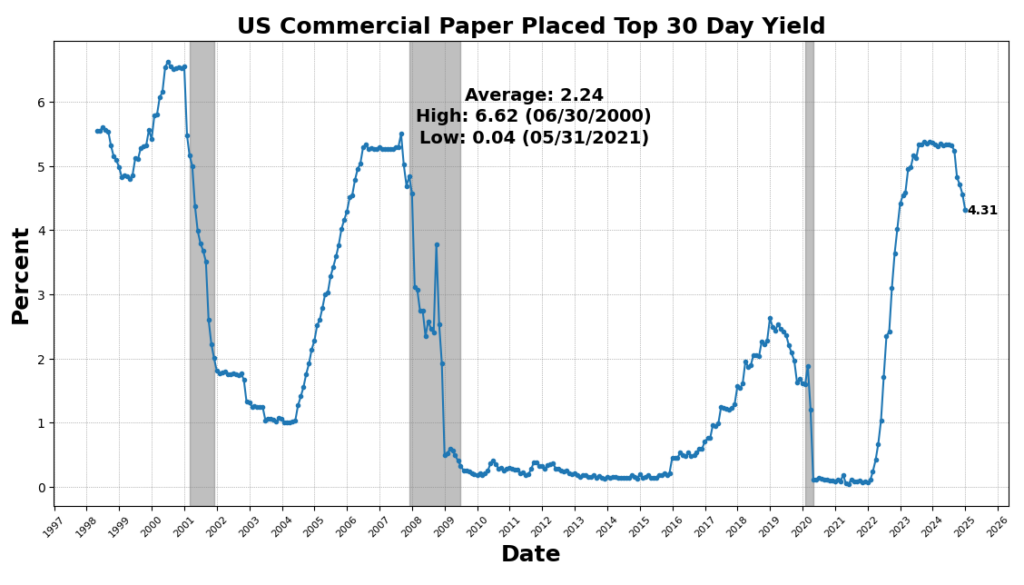

The one unchanged measure was US Business Paper Positioned Prime 30 Day Yield, indicating secure short-term credit score circumstances. The Convention Board’s Lagging Common Period of Unemployment fell 7.2 %, suggesting that unemployed people are discovering jobs sooner, a optimistic signal for the labor market.

The January 2025 AIER Enterprise Circumstances Month-to-month indicators mirror an economic system nonetheless increasing however extra slowly and with combined indicators. The decline within the Main Indicator from 71 to 54 was pushed by weakening client sentiment, slowing retail and meals companies gross sales, stagnation in manufacturing exercise, and strain from each a deteriorating housing market and tightening monetary circumstances.However that the Roughly Coincident Indicator (67) remained stable, and the Lagging Indicator (83) improved notably, indicating power in slower-moving financial elements like inflation, credit score, and labor market restoration.

The divergence between main and lagging indicators makes the quickly escalating uncertainty in forward-looking financial circumstances clear, although real-time and lagging measures recommend areas of ongoing resilience. The twin risk of untamed, last-minute coverage fluctuations forward of April 2nd and the long-term penalties of what might be the biggest tariff improve because the Smoot-Hawley Act of 1930 at the moment are the first forces shaping financial exercise and monetary market conduct.

DISCUSSION

February’s CPI report highlighted the results of weakening client demand for discretionary items, reinforcing broader indicators of softening consumption. Whereas companies disinflation continued, items value declines stalled, notably in classes delicate to tariffs together with automobiles, house furnishings, and attire. The general affect of President Trump’s commerce insurance policies on inflation will rely on whether or not weaker companies spending offsets rising items costs. For now, the February knowledge means that companies disinflation outweighed the modest uptick in items inflation, delaying any vital reacceleration in value development.

US wholesale inflation stagnated in February, as a 1 % decline in commerce margins offset rising prices in key sectors, tempering the general producer value index (PPI), which remained unchanged from January’s revised 0.6 % achieve. Excluding meals and vitality, PPI declined for the primary time since July, although underlying value pressures continued, notably in classes tied to the Federal Reserve’s most well-liked inflation gauge, the private consumption expenditures (PCE) value index. Hospital inpatient care prices rose 1 %, portfolio administration charges elevated 0.5 %, and core items costs (excluding meals and vitality) climbed 0.4 %—the biggest month-to-month achieve in over two years. Whereas declining wholesale margins could briefly protect customers from increased import and manufacturing prices, sustained weak client confidence and pulled-forward sturdy items purchases might weaken demand later this 12 months, probably forcing retailers to simply accept thinner revenue margins. Tariffs imposed by the Trump administration are additionally set to exert upward value pressures, with a further 10 % levy on Chinese language imports launched in February contributing to notable value good points in iron and metal scrap, equipment, and family items like furnishings and home equipment. In the meantime, meals costs surged 1.7 %, pushed by rising egg prices, whereas vitality costs fell 1.2 %. Regardless of these combined inflation indicators, a separate report confirmed jobless claims remained secure, reinforcing the resilience of the labor market.

February value knowledge confirmed broad-based will increase in each manufacturing and companies, with a number of regional and nationwide surveys reflecting stronger pricing energy throughout industries. The ISM Manufacturing Costs Index surged to 62.4, its highest degree since June 2022, up from 54.9 in January, whereas ISM Providers Costs remained elevated at 62.6. S&P World’s US Manufacturing sector recorded its quickest output value development in two years, whereas US Providers companies raised costs modestly, constrained by aggressive pressures and weak demand. Regional Federal Reserve surveys additional confirmed rising value pressures, with the Kansas Metropolis Fed reporting a 3rd consecutive month of value good points in manufacturing, and its non-manufacturing sector additionally seeing increased promoting costs. The New York Fed’s manufacturing costs acquired index jumped to 19.6 from 9.3, practically doubling its six-month common, whereas its companies counterpart climbed to 27.4 from 19.4. Equally, the Philadelphia Fed’s manufacturing index elevated to 32.9 from 29.7, whereas the Dallas Fed’s manufacturing costs acquired measure rose to 7.8 from 6.2. The Chicago PMI indicated an acceleration in value enlargement, and the Richmond Fed’s manufacturing index confirmed a modest uptick, with costs acquired rising to 1.62 from 1.21.

Whereas value pressures had been broadly increased, choose areas noticed moderation. The Dallas Fed’s companies sector reported a decline in promoting costs, falling to 7.9 from 13.7, and the Philadelphia Fed’s non-manufacturing costs acquired index turned destructive, dropping to -1.1 from -0.3. Richmond Fed companies costs edged decrease to three.31 from 3.55. Total, the info suggests persistent inflationary pressures, notably in goods-producing sectors, with some indicators of value reduction in companies. This helps a combined inflation outlook, with value development accelerating in manufacturing and remaining agency in companies, regardless of remoted cases of easing.

Job development in February 2025 exceeded expectations, with nonfarm payrolls rising by 151,000, led by good points in development, manufacturing, well being care, monetary actions, transportation, and social help, whereas declines occurred in leisure and hospitality, retail, and authorities employment, notably on the federal degree resulting from a hiring freeze. The common workweek remained regular at 34.1 hours, contributing to a 0.3 % improve in weekly earnings. Nonetheless, labor market slack widened, with the unemployment price (U-3) rising to 4.14 %, reflecting a rise of 203,000 unemployed people. The U-2 price, which tracks job losses, additionally climbed, whereas the broader U-6 measure of underemployment surged to eight.0 %, indicating an increase in discouraged and involuntarily part-time employees. The labor pressure participation price dipped to 62.4 % as employment declined by 588,000, and transitions out of unemployment slowed, signaling weaker hiring momentum. Combination labor revenue rose 0.4 %, largely on wage development, however indicators of labor market softening—notably increased unemployment, an increasing pool of job seekers, and slower re-employment—reinforce expectations for a 75 foundation level price lower by the Federal Reserve in 2025 as financial circumstances deteriorate.

US client sentiment fell sharply in early March, reaching its lowest degree since November 2022, as issues over tariffs and financial uncertainty weighed on confidence. The College of Michigan’s preliminary sentiment index declined to 57.9 from 64.7 in February, marking a steeper drop than any economist forecasted. Lengthy-term inflation expectations surged by 0.4 share level to three.9 %, the biggest month-to-month improve since 1993, whereas one-year inflation expectations rose to 4.9 %, the very best since 2022. As President Trump’s tariffs broaden, customers throughout the political spectrum more and more worry rising prices, with 48 % of survey respondents mentioning tariffs unprompted, anticipating them to drive future inflation increased. Households’ monetary expectations hit a report low, and respondents assigned only a 48.7 % chance to inventory market good points over the following 12 months, the weakest studying since Might 2023.

Deteriorating confidence presents a rising danger to client spending, notably in big-ticket purchases like houses, autos, and discretionary items. The present circumstances gauge fell to 63.5, a six-month low, whereas the expectations index dropped to its lowest degree since July 2022. Political divisions had been evident, with confidence amongst Democrats falling practically 10 factors, independents down 5.4 factors, and Republicans slipping practically 3 factors. Economists warn that elevated uncertainty over coverage shifts and financial circumstances is making it tough for customers to plan for the longer term, reinforcing fears that slowing confidence might curb family spending and contribute to financial draw back dangers within the months forward.

Small-business optimism declined in February as inflation, coverage uncertainty, and issues over tariffs weighed on sentiment. The NFIB Small Enterprise Optimism Index fell 2.1 factors to 100.7, barely beneath expectations, with the sharpest declines in financial outlook (-10 factors), anticipated gross sales (-6 factors), and enlargement plans (-5 factors). Whereas job openings (+3 factors), earnings tendencies (+1 level), and anticipated credit score circumstances (+1 level) improved, general optimism stays nicely beneath December’s peak of 105.1, although nonetheless increased than the pre-election degree of 93.7 in October. Hiring plans softened, with solely 15 % of householders planning so as to add jobs within the subsequent three months, down 3 factors from January, as retail, development, and manufacturing confronted the best labor shortages. Simply 19 % of companies plan to broaden within the subsequent six months, reflecting decrease anticipated gross sales (14 %, down 6 factors) and weak profitability tendencies (-24 %). Inflation pressures intensified, with 32 % of companies elevating costs, a 10-point bounce and the biggest improve since April 2021, although companies held off on preemptive pricing changes forward of tariffs. Regardless of tax cuts and deregulation boosting the long-term outlook, excessive uncertainty is protecting small companies in a wait-and-see mode, limiting hiring and enlargement.

February retail gross sales fell in need of expectations, reinforcing issues a few slowdown in client spending, whereas weaker manufacturing and homebuilder sentiment additional signaled softening financial momentum. Retail gross sales rose marginally, however seven of the 13 classes declined, together with motor autos, electronics, attire, and gasoline, with restaurant and bar gross sales posting their sharpest drop in a 12 months. January’s figures had been revised downward, marking the biggest decline since July 2021. Whereas e-commerce exercise and healthcare spending lifted control-group gross sales by 1 %, economists famous that seasonal changes performed a major function, limiting optimism for first-quarter GDP. Weaker revenue development and rising job insecurity are probably curbing discretionary spending, notably amongst lower-income customers, whereas wealthier households may additionally in the reduction of on main purchases following latest inventory market volatility. Enterprise warning is rising as New York state manufacturing exercise dropped to its lowest degree since early 2024 and homebuilder confidence fell to its weakest studying since August. Mounting uncertainty over tariffs, slowing wage development, and deteriorating client sentiment improve the probability of weaker financial enlargement, with some analysts warning that first-quarter GDP development might contract.

US manufacturing exercise in February edged nearer to stagnation, with orders and employment contracting whilst enter prices surged. The ISM Manufacturing Index slipped 0.6 factors to 50.3, whereas costs paid for supplies jumped 7.5 factors to 62.4, the very best since June 2022, signaling renewed inflationary pressures. New orders fell 6.5 factors to 48.6, the primary contraction since October 2024, and manufacturing facility employment dropped 2.7 factors to 47.6, marking contraction in eight of the previous 9 months. Rising prices, largely pushed by tariff-related provide disruptions, are creating backlogs and stock imbalances, with companies struggling to cross on value will increase amid softening demand. Imports climbed to 52.6, the very best since March 2024, as companies ramped up orders forward of Trump administration tariffs on Mexico and Canada set to take impact Tuesday. In the meantime, headline industrial manufacturing surged 0.7 %, largely resulting from a 4.3 % bounce in client sturdy items output, led by a pointy rise in automotive manufacturing. Manufacturing manufacturing expanded 0.9 %, whereas enterprise gear output rose 1.6 %, persevering with its sturdy development since November. Capability utilization elevated to 78.2 % from 77.7 %, as factories ramped up exercise. The surge in manufacturing could mirror companies front-loading output earlier than tariffs disrupt provide chains, suggesting a possible slowdown forward. Nonetheless, with Trump administration insurance policies targeted on onshoring and boosting home manufacturing, industrial exercise could proceed to obtain reasonable tailwinds regardless of near-term volatility.

In February and early March of 2025 the US economic system confirmed combined circumstances. Reasonable client spending development, secure automobile gross sales, and resilience in monetary companies had been evident however clear indicators of pressure in manufacturing, development, and agriculture have gotten clear. Vacation retail gross sales exceeded expectations, and nonfinancial companies, together with leisure, hospitality, and transportation, expanded modestly, notably in air journey. Business actual property noticed slight good points, and lending exercise remained regular with little deterioration in asset high quality. Nonetheless, development exercise declined as excessive materials and financing prices dampened development, and residential actual property remained stagnant resulting from elevated mortgage charges. Manufacturing slipped barely, with companies stockpiling inventories in anticipation of upper tariffs and truck freight volumes fell, signaling weaker items demand. Rising delinquencies amongst small companies and lower-income households raised issues about monetary stability and the general disposition of customers. Agricultural circumstances remained weak, with low farm incomes and climate disruptions including strain.

The large surge in client and enterprise optimism seen in November 2024, pushed by disinflationary progress and powerful company expectations of pro-business insurance policies has steadily eroded within the face of skyrocketing uncertainty. By February and early this month cussed inflation, weakening employment tendencies, and clear indicators of client misery have fueled a pointy reversal in sentiment. Report ranges of coverage instability—marked by an unprecedented tempo of govt orders, shifting tariff threats, and mounting regulatory uncertainty—has additional compounded financial unease, disrupting enterprise planning and funding. With the Trump administration’s full slate of tariffs set to take impact on April 2nd, commerce flows, enter prices, and company methods face the potential for vital upheaval.

With companies and households more and more transferring to the sidelines amid mounting financial uncertainty, issues over the probability of a recession have risen sharply. Public discourse on the topic has intensified, and whereas the last word consequence stays unsure, these issues might not be untimely. Given the present coverage and financial panorama, sturdy warning is warranted.

LEADING INDICATORS

ROUGHLY COINCIDENT INDICATORS

LAGGING INDICATORS

CAPITAL MARKET PERFORMANCE

– Neural Networks – 4 November 2025")

{kind=link}