Josh Hendrickson has a brand new Substack put up that discusses the implications of the US greenback’s function as a global reserve foreign money. This caught my eye:

If you find yourself taught a typical mannequin of worldwide commerce with versatile alternate charges, dialogue of the steadiness of commerce goes one thing like this. If a rustic runs persistent commerce deficits, its foreign money will start to depreciate. The depreciation of the foreign money makes overseas items costlier. This tends to cut back imports and push the nation towards balanced commerce. The fundamental level right here is {that a} typical textbook argument is that versatile alternate charges modify to the steadiness of commerce and these changes have a tendency to cut back the commerce deficit and push the nation in the direction of balanced commerce.

Against this, the U.S. runs persistent commerce deficits that don’t self-correct. In actual fact, many instances, the greenback appreciates whereas the U.S. is operating commerce deficits. How can we clarify this phenomenon?

The rationale that the U.S. is completely different is that the greenback is the first foreign money utilized in international commerce.

Two feedback:

The US isn’t completely different.

Josh Hendrickson ought to get a brand new textbook.

Right here’s the US present account as a share of GDP:

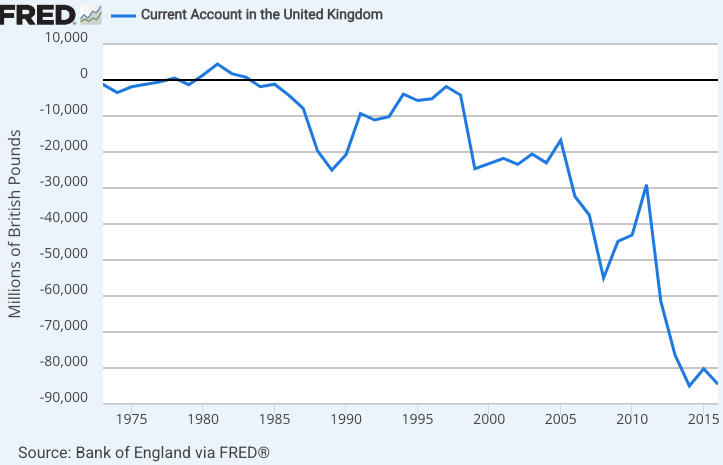

Now let’s have a look at Nice Britain:

Sadly, the British FRED collection ends in 2016 and is in cash phrases, not share of GDP. Nevertheless, one other supply confirms the UK present account deficits have continued at roughly 3% of GDP.

And right here’s New Zealand:

And right here’s Australia:

In equity, a newer Fred collection exhibits a short interval of surplus, earlier than returning to deficit in 2024:

In actual fact, the US is pretty typical of English-speaking nations that draw numerous immigration—it runs pretty persistent deficits. The outlier is Canada, which ran present account surpluses from 1999-2008, however even they’ve seen present account deficits for the previous 16 years, and 52 of the previous 65 years.

A present account steadiness merely displays the distinction between saving and funding; there’s no cause why it can not proceed indefinitely. It might be related to extreme borrowing, particularly extreme authorities borrowing, however that isn’t all the time the case. (Australia tends to have small price range deficits.)

The US present account deficits are most likely attributable to the identical form of components that designate present account deficits in different English-speaking nations: low saving charges, extremely productive capital investments and excessive charges of immigration. I see no proof that the greenback’s function as a reserve foreign money performs a lot of a task, until you imagine that the New Zealand greenback can be an necessary reserve foreign money.

Hendrickson continues:

The quick reply is that different nations must be internet importers of {dollars} and due to this fact internet exporters to the U.S.

What this suggests is that the U.S. should run persistent commerce deficits with the remainder of the world to be able to present the world with {dollars}.

This isn’t correct. A present account deficit shouldn’t be a internet circulate of {dollars}; it’s a internet circulate of property. We might pay for imports by promoting actual property or equities or junk bonds. A overseas nation might accumulate US greenback reserves (Treasuries) by promoting property like shares or actual property or overseas authorities bonds.

The US present account deficit displays the discrepancy between home saving and home funding. The US shouldn’t be “pressured” to run a deficit, even with the greenback serving as a global reserve foreign money.

I don’t fear about present account deficits, but when the Trump administration needs to deal with the problem then they need to take into account lowering the federal government price range deficit (which is unfavorable saving.) As an alternative, they’re planning to enact a large tax reduce. A recession may additionally scale back the present account deficit, by lowering home funding.

PS. I’m not sure why Australia’s present account has not too long ago develop into extra optimistic; maybe it displays a cultural change related to in depth immigration from (excessive saving) Asian nations. However that doesn’t clarify Canada.

")

{kind=link}